FX News Today

- Stock markets remained supported during the Asian session after a higher close on Wall Street yesterday.

- The prospect of a new round of trade talks helped to underpin sentiment Thursday and investors are scaling back easing expectations for the upcoming ECB and Fed meetings.

- Markets priced out a lot of their easing expectations for next week’s ECB meeting yesterday, the German production number (German industrial production fell -0.6% m/m in July,) acted as a reminder that the balance of risks still remains tilted to the downside and that also holds for Brexit risks.

- US reports revealed a surprisingly large August ISM-NMI bounce to 56.4 from a 3-year low of 53.7, alongside a similar ISM-adjusted bounce to 56.1 from a 3-year low of 53.0. The employment gauge fell, however, to a 2-year low of 53.1 from 56.2.

- The confidence in progress on the trade front is far from secured yet and while yesterday’s private payroll survey in the US was better than expected, markets are holding back ahead of official US Payroll numbers later today.

- Nikkei (JPN225) rose 0.43%. The Shanghai Comp is up 0.06%.

- European stock futures posted slight losses, while US futures held on to fractional gains.

- The USOIL meanwhile is trading at $56.30 per barrel.

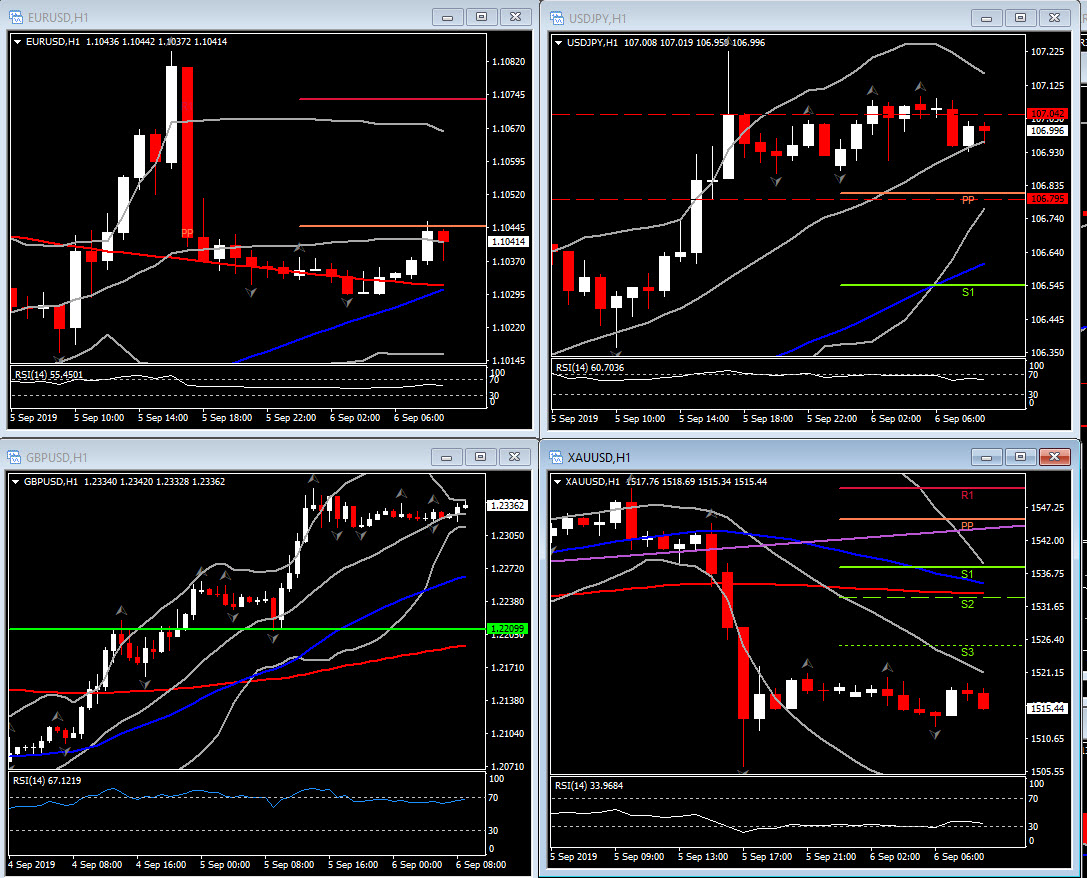

Charts of the Day

Technician’s Corner

- EURUSD rallied early in the session topping at 1.1085, right at its 20-day moving average. Gains came on risk-on conditions, along with the market’s apparent scaling back of ECB easing expectations. Later, a stronger ADP jobs report and firmer services ISM reversed the pairing’s course, as the Dollar turned broadly higher on the data. The Euro later eased back toward 1.1035 before steadying. Relative strength of the US economy over Europe should keep EURUSD in sell-the-rally mode going forward.

- USDJPY has rallied sharply, peaking at 107.22 yesterday, levels last seen on August 2, and above its 50-day moving average for the first time since August 1. Prospects for US/China trade talks in October, along with better US data, and the accompanying Wall Street and Treasury yield rallies, have supported the pairing through the morning session. Currently is moving sideways in the upper BB (1-hour chart) and within the 1-month Resistance area at 106.80-107.04. A decisive daily candle above this area could turn the overall outlook.

Main Macro Events Today

- UK court hearing on forcing no-deal Brexit

- Gross Domestic Product (EUR, GMT 09:00) – Eurozone’s economic growth s.a for Q2 2019, is likely to remain confirmed with GDP rising by 0.2% q/q.

- NFP and Labour Market Data (USD, GMT 12:30) – A 155k August nonfarm payroll rise has been estimated, following a 164k increase in July. The unemployment rate should tick down to 3.6% after an uptick to 3.7% in June that was sustained in July, and hours-worked are estimated to rise 0.3%. Average hourly earnings should rise 0.3% m/m.

- Employment Change (CAD, GMT 12:30) – Employment change is seen spiking to 12.5k in the number of employed people in August, compared to the decline 24.2k in July. The unemployment rate is expected to remain at 3.7%.

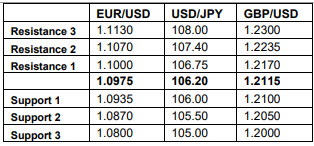

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.