FX News Today

- Treasury yields declined overnight, as sentiment improved and central bank decisions come into view.

- Stock markets remained supported during the Asian session as trade jitters continue to ease.

- Bolton’s departure in the US has triggered renewed hopes of a softer stance in the Trump camp and goodwill gestures from both China and the US have rekindled hopes that tensions can be resolved through talks after all.

- President Trump said he will delay the next US tariff increase on China by about two weeks, after China yesterday published an exemption list of its own tariffs on US imports.

- The final reading of German August HICP inflation brought no surprise, with HCIP confirmed at just 1.0% y/y, far below the ECB’s reference rate of 2.0%.

- US and European futures are moving higher.

- The WTI future is trading at USD 56.27 per barrel.

- The focus meanwhile is turning to today’s ECB meeting, which is widely expected to bring a cut to the deposit rate, but could disappoint on the QE front and coming ahead of the Fed decision next week, many will see it as a bellwether for easing intentions at global central banks.

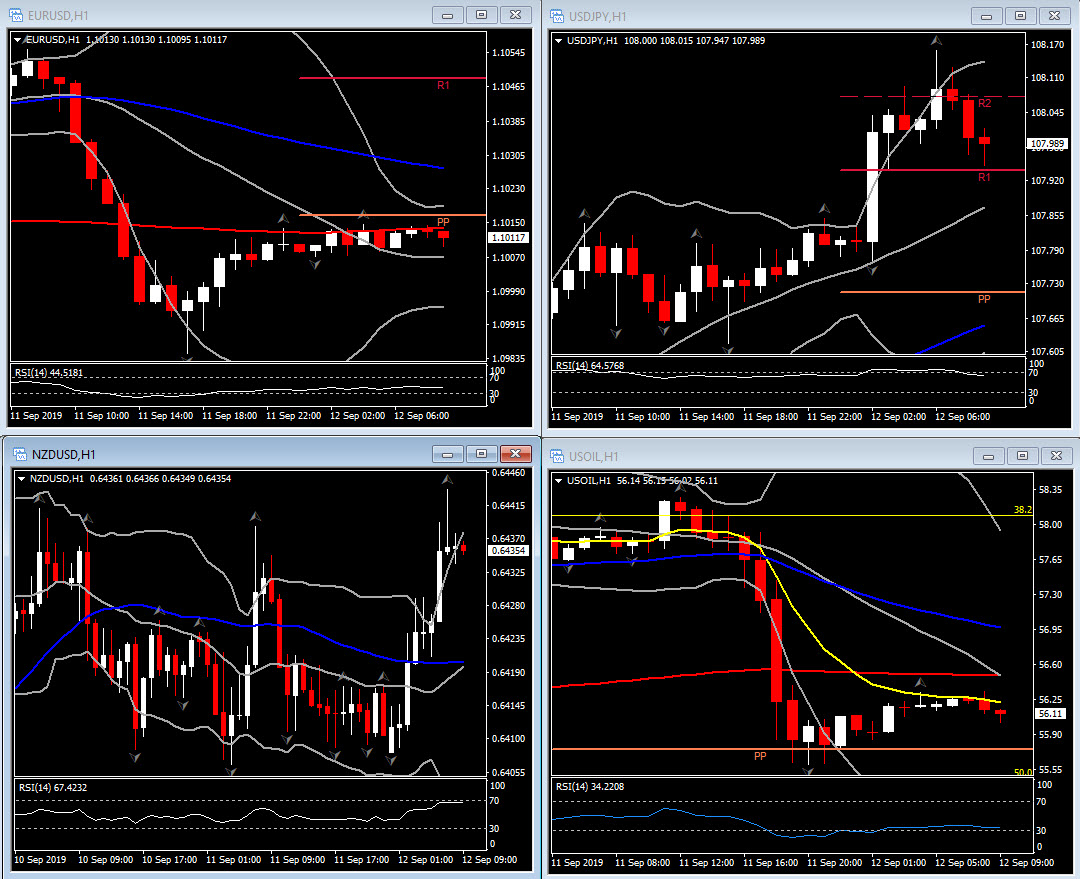

Charts of the Day

Technician’s Corner

- The Dollar saw a 6-week high against the Yen, as goodwill gestures from both the US and China on the tariff front lifted risk appetite. The Yen continued to see its safe-haven premium deflate. USDJPY is trading over 108, in what is now a fourth consecutive day of ascent, which is in turn amid a third consecutive week of gains. AUDJPY and GBPJPY also continued to rise amid general strength in export-driven currencies amid the buoyant mood on the trade front.

Main Macro Events Today

- Interest Rate Decision, Monetary Policy Statement and Press Conference (EUR, GMT 11:45 & 12:30) – The ECB is expected to cut deposit rate by 10 bp to -0.50%, with new tiered system to limit the impact. Most analysts are expecting a 10 bp cut in the deposit rate, which would leave it at -0.50%. The repo rate, currently at 0.00%, is likely to be kept on hold for now. The ECB is anticipated to re-open QE. There even is a risk that the restart of QE will be put on hold for now. With Lagarde taking over from Draghi in November, the pressure on governments to open their purse strings and complement an expansionary monetary policy with fiscal measures will likely increase.

- Consumer Price Index and Core (USD, GMT 12:30) – The headline August CPI is estimated flat with a 0.2% core price increase, following July readings of 0.3% for both. As-expected gains would result in a headline y/y increase of 1.7%, down from 1.8% in July, while core prices should rise 2.3% y/y, up from a 2.2% pace in July. Overall, the inflation outlook remains benign, though we do expect an up-tilt in y/y gains into Q1 of 2020 due to harder comparisons.

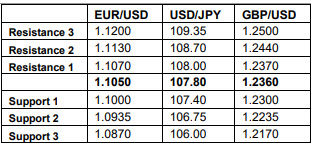

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.