Judging by preliminary readings out of Spain and Italy, and German state inflation numbers released so far today, Eurozone inflation is likely to drop again in September. All showed a marked deceleration in the annual rate as did the French preliminary inflation data released last Friday. Based on the numbers so far we have revised down our forecast for the overall Eurozone number (due Tuesday) to 0.8% y/y, from 1.0% y/y expected previously. A further decline in the headline rate will add to the number of releases that seemed to vindicate Draghi’s decision to deliver further easing measures and will likely see the central bank continuing to stress that the central bank remains open to taking additional steps if necessary.

Meanwhile, we have seen the release of labor and retail sales data from Germany. German sa jobless numbers unexpectedly fell -10K in September, the first decline since April. The jobless rate remained steady at a very low 5.0% – as expected. The number of open jobs continued to decline, however, and despite the positive surprise in the September reading, surveys make it pretty clear that companies are increasingly reluctant to take on more staff as orders inflow slows. So it still seems only a matter of time until the jobless rate starts to move higher, especially as the balance of risks remains tilted to the downside, with global trade tensions and Brexit uncertainty hitting not just the manufacturing sector.

On the flipside, German retail sales rose 0.5% m/m in August, slightly less than we had hoped but in line with Bloomberg consensus. The annual rate came in higher than anticipated, as July readings were revised sharply higher – to show a contraction of just -0.8% m/m, a much better result than the -2.2% m/m reported initially. Although the latest improvement in consumer confidence offers a glimmer of hope, the fact that the improvement in jobless numbers has run out of steam will likely limit private spending going forward.

The data have not significantly changed the Euro’s mood so far today. Euro remains mixed, with Sterling being the gainer of the day and Kiwi, Swiss the losers.

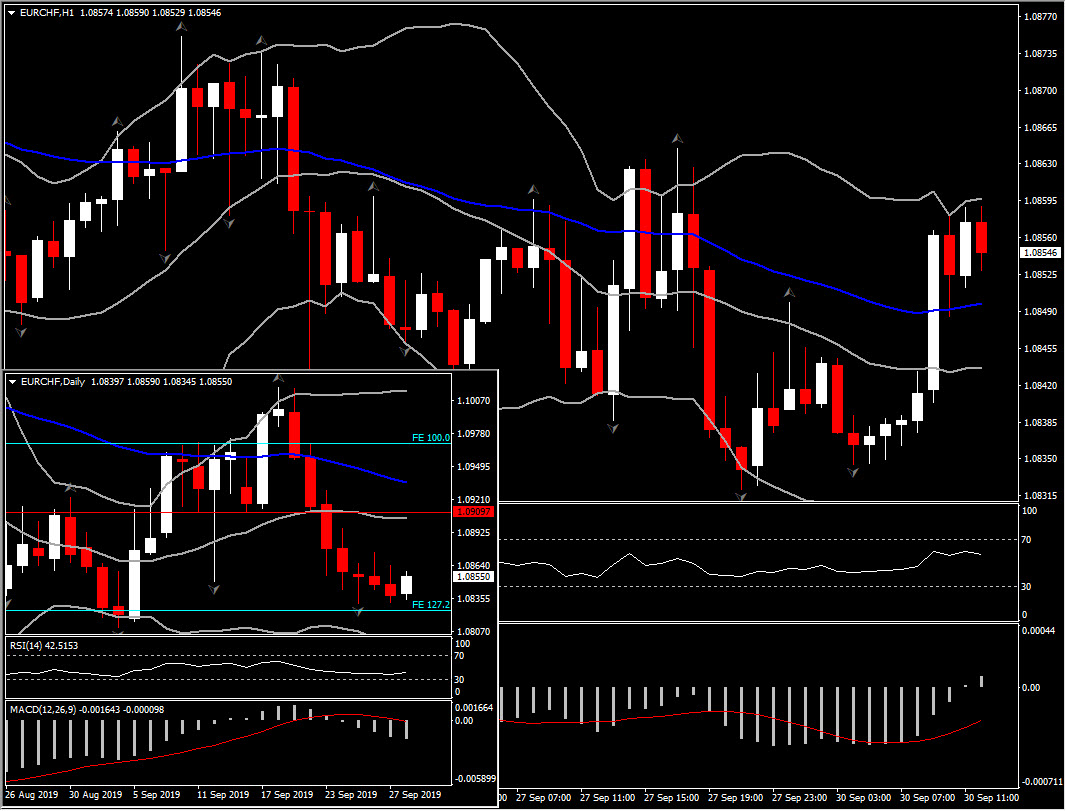

EURCHF has found a toehold after about a week-long spell of underperformance, which culminated in a 3-week high being printed last Wednesday at 1.0832. The declines followed the SNB’s quarterly policy announcement last week, which will be frustrating to Swiss policymakers given their chronic concerns regarding the Franc’s chronic state of overvalue-ment (which regularly tops the Economist magazine’s Big Mac purchasing parity comparison of currencies). The 26-month high seen in early September at 1.0811 has so far remained untroubled, but still looks vulnerable. Currently the asset has jumped to the 1.0868 area, with the next Resistance between Thursday’s high and 50-period EMA (H4), at the 1.0875-1.0880 area. Support holds at 1.0850. A break of the 1.0880 level could turn the near picture from neutral to a positive one.

Additionally, Sterling has traded firmer, reversing some of the losses seen last week. EURGBP concurrently descended, and GBP concurrently ascended. Brexit remains front and centre. Opposition parties, led by Scotland’s SNP, are looking to stage a confidence motion as soon as this week to take down Boris Johnson’s government, concerned that he might on a technicality disregard the new law (the Benn bill) preventing a no-deal Brexit on October 31 in the event that a deal has been achieved. This hasn’t until now been looking like a viable option given that the opposition have been divided about who would lead an interim government, with leader of the opposition, Labour’s Corbyn, unpopular. In the event this happens, a delay in Brexit to January 31 would be all but assured, with a general election likely in late November.

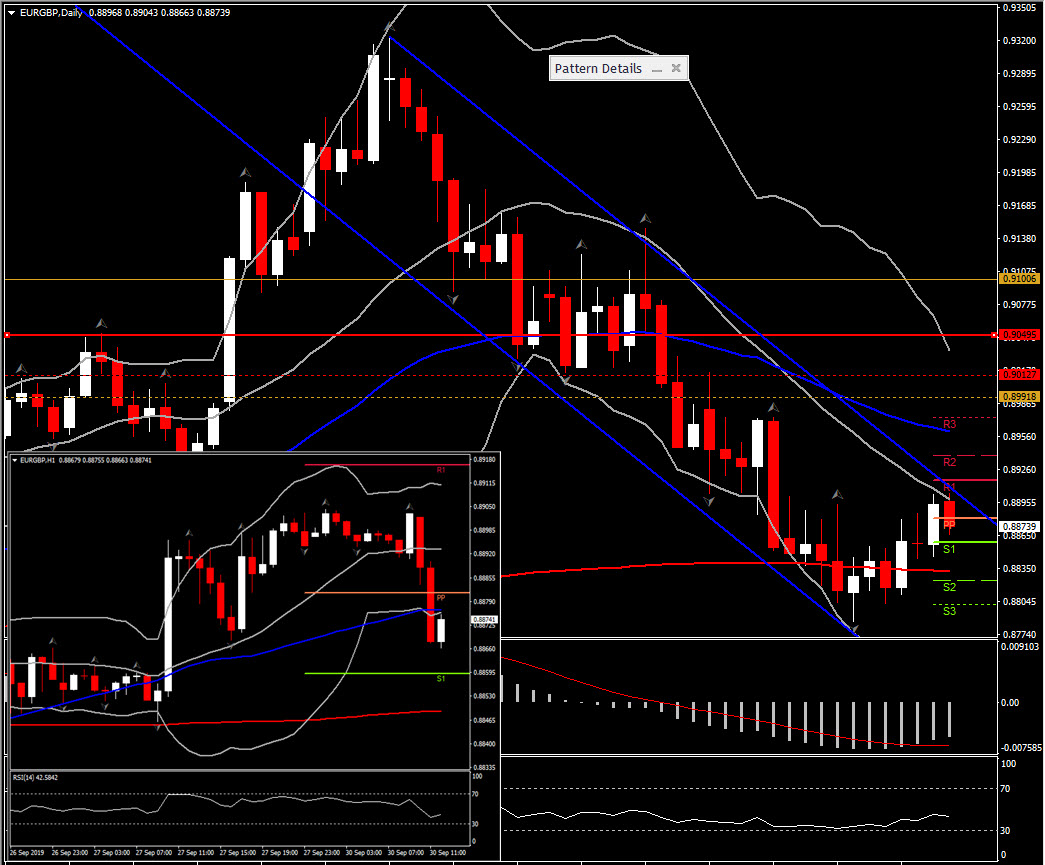

From a technical perspective, EURGBP retested the 0.8900 level for a 2nd day which is interestingly the 50% Fib. level since May’s rebound, before reversing lower. In the European session though the pair found some wings again. The intraday momentum indicators are leading the market into a possible continuation of this recovery, with MACD holding above neutral and RSI looking to the upside.

However, only a clear cross above the key level at 0.8900 could support a positive outlook for EURGBP in the medium term.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.