Canada’s lack of GDP growth in July was driven by temporary factors impacting Oil and gas extraction, although broadbased declines across the other goods sectors suggest trade frictions did have a negative impact.

Goods sector output fell 0.7% in July, led lower by a 3.5% tumble in mining, quarrying and oil and gas extraction that was the largest one month drop since May of 2016. A 3.0% tumble was seen in oil and gas extraction, with Statistics Canada noting that oil and gas extraction ex-oil sands plunged 4.7%, the largest decline in a decade. However, that was largely due to the shutdown of some of Newfoundland and Labrador’s offshore production facilities for much of the month due to maintenance issues.

Construction fell 0.7% after a 0.6% gain, manufacturing dipped 0.1% after a 1.3% pull-back. Service producers grew 0.3%, matching the 0.3% rise in June, supported by a robust 1.1% rise in wholesale production. Retail shipments edged up just 0.1% after a 0.6% expansion.

The lack of total GDP growth in July undershot expectations for a modest rise, but the undershoot can be attributed to what should be a temporary set-back in oil and gas. Yet softness in manufacturing, construction and retail support the BoC’s currently accommodative policy stance. Of course, the BoC anticipates a moderation in GDP during the second half of this year, and today’s GDP report supports that projection.

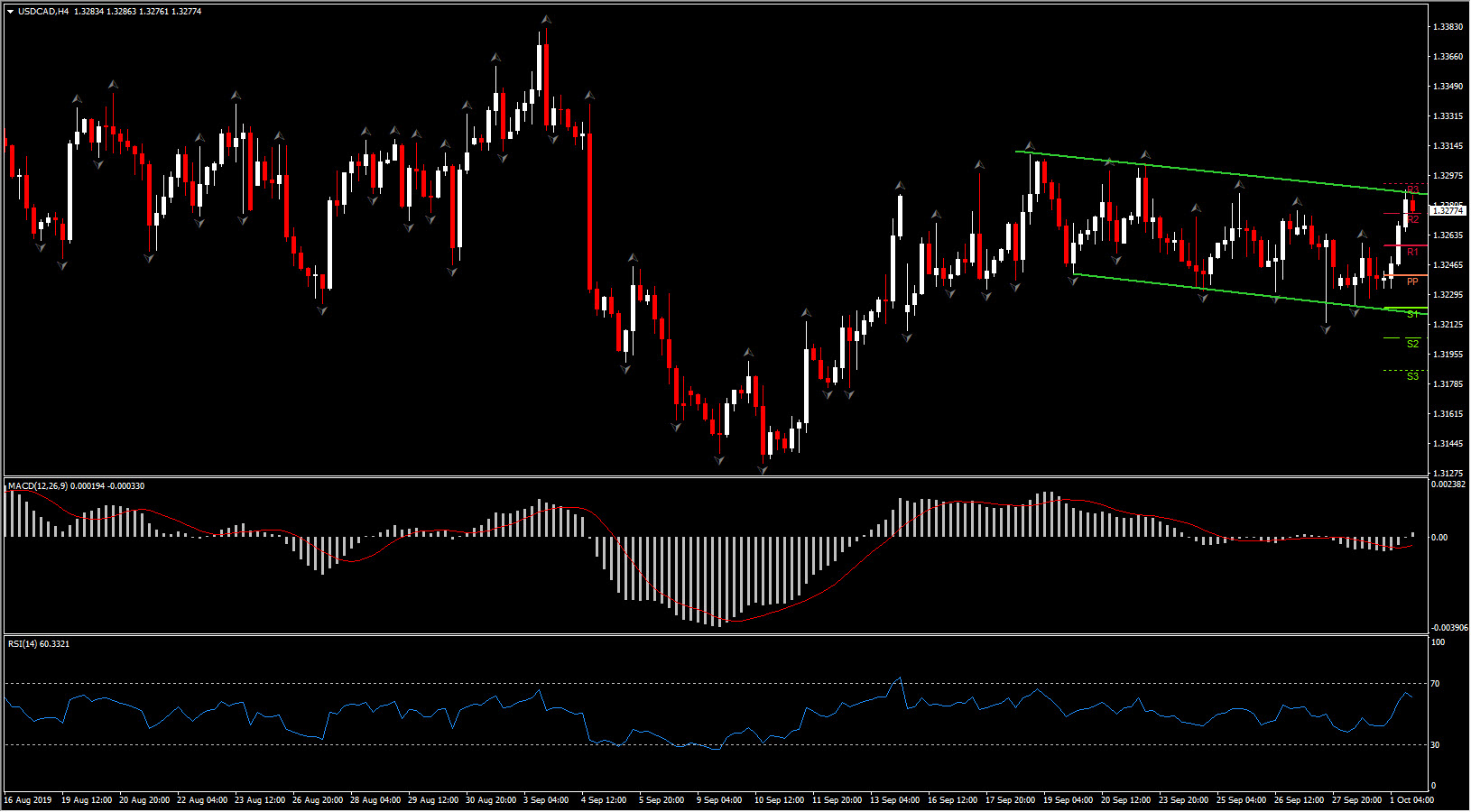

From the currency perspective, USDCAD has recouped back above 1.3250, a level that the pair has been gravitating around for over a week now. Oil prices have steadied after more than giving back the sharp gains seen in the immediate wake of the attack on Saudi crude facilities.

Other than the GDP, there are some key data loom on both the US and Canadian calendars this week. The US schedule culminates in the release of the September jobs report on Friday. The risks relative to expectations are clearly to the downside regarding upcoming US economic reports, which generating downside bias in USDCAD. As for Canadian data, trade balance is expected to show a narrowing in the deficit to -C$1.0 bln in August from -C$1.1 bln in July.

Overall, assuming oil prices remain capped, and assuming incoming US versus Canadian data maintains a slight dovish gap in Fed versus BoC outlooks, USDCAD’s looks likely to retain a moderate downward track, with ups and down forming a downchannel.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.