The markets were crushed, and especially bonds, as a hotter than expected CPI and hawkish comments from Bullard weighed heavily on the markets. The 7.5% y/y pace of CPI, a 40-year high, boosted concerns that the FOMC will have to take a more aggressive stance on rate hikes and tightening down the road. But the nail in the coffin were comments from the Fed hawk Bullard who said he now advocated for a half point rate increase in March and 100 bps of tightening over the first half of the year. The UK economy grew by 7.5% last year despite Omicron causing slowdown. Treasury yields soared with the 10-year cheapening through the 2.0% level for the first time since July 31, 2019. Wall Street was hammered too and the major indexes plunged on the day.

- USD (USDIndex rallied to 96.00).

- US Yields sharply higher, spiked further, leaving the 2-year rate up 25 bps to 1.579% – biggest single daily move since June 2009 and the great financial crash. The 10-year was up 10 bps at 2.029%, closing with a 2% handle for the first time since July 31, 2019.

- Equities were led by the -2.10% drop in the USA100, while the USA500 was -1.81% lower, with the USA30 down -1.47%. Tech stocks have been hit by the prospect of accelerated Fed hikes and GER30 and UK100 are currently down -1.3% and -1.0%.

- Earnings: Affirm stock dropped 21%. Twitter unchanged, as Twitter’s mixed fourth quarter shows its challenges ahead, PepsiCo down by 2.1%, beat earnings but warns on costs while full-year outlook fell short. Disney 3.50% up, shows rebound in Disney+ & Parks businesses.

- USOil – at $88.00 following a spike at 90.60.

- Gold – down to $1820.90.

- Bitcoin settled to $43,000 – 44,000 area.

- FX markets – USD on bid as yields spiked and USDJPY jumped to 116.32, although the Yen strengthened against most other currencies as risk appetite waned. AUD and NZD drifted. EURUSD declined to 1.1370 & Cable down to 1.3512.

European Open – The March 10-year Bund future is down -23 ticks, but the 30-year future has rallied and US futures have found a footing. So there are some signs of stabilisation at least at the long end. EGBs sold off yesterday in the wake of the higher than expected inflation print, and while the UK curve shifted higher across the board, thanks to Lane’s dovish comments on the policy outlook, the short end outperformed in the Eurozone and the curve steepened as the long end sold off, with Italian BTPs once again hit most.

Today – Today’s calendar is light, with just the preliminary University of Michigan consumer sentiment index due. Today’s earnings calendar features reports from Enbridge, Dominion Energy, Magna International, and Fortis.

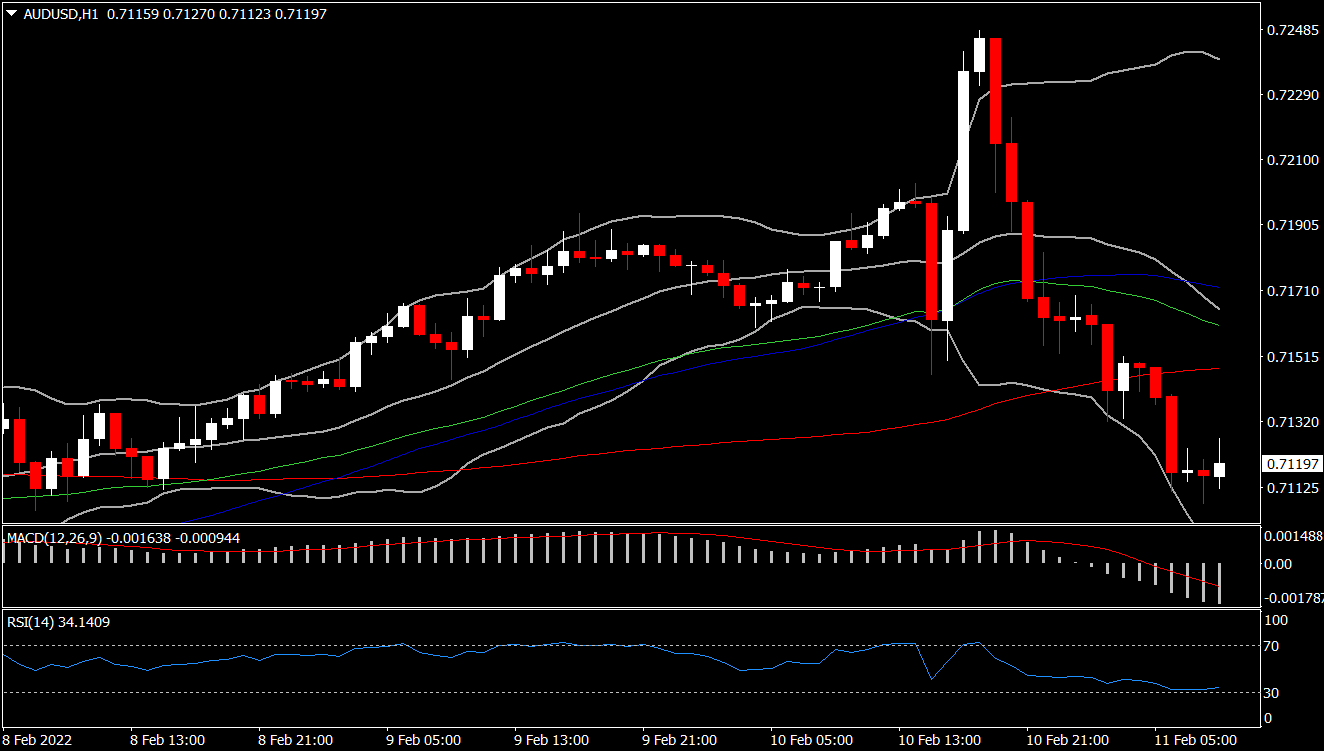

Biggest FX Mover @ (07:30 GMT) AUDUSD (-0.58%) – Dipped to 0.7110 on USD strength. Fast MAs currently flat, as MACD signal line & histogram extend southwards and RSI at 36, indicating near term consolidation and overall pressure.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.