US Stock markets crashed into close (US30 -622pts) after a weak day. US data biased lower (Philly Fed 16.0 vs 23.2, Initial Claims 248K vs 217k & Housing data mixed.) USD cools on its safe-haven bid. Gold rallied to test $1900, Oil remained under $90.00, Yields widened again but remain elevated. Asian markets also slipped (Nikkei -0.43%, ASX worst performer -1.0%.) Claims & counterclaims yesterday over who fired on who, Russia expelled a US diplomat and today there are reports of 30 more troop and tank withdrawals; also “provided there is no further Russian invasion of Ukraine,” Blinken & Lavrov will meet late next week.

- USD (USDIndex 95.75) consolidating in range; Wednesday’s & last Friday’s low 95.65.

- US Yields 10-yr cooled into closed 1.97% and trades lower today, 2-yr remains elevated.

- Equities – USA500 -95 pts (-2.12%) 4380 – (NVDA -7.56%, FB -4.02% TSLA -5.0%, WMT + 4.01% (Big Earnings beat & Divi increase)- US500 FUTS recover to 4396, currently.

- USOil – Topped at $91.00, back to under $90.00 now and trades at $89.20 now. Wednesdays & last Friday’s low 88.00.

- Gold – Rallied through psychological $1900 earlier to test 2021 highs, now back to $1892

- Bitcoin broke out of the $42k-45K range and trades down to test $40K.

- FX markets – EURUSD pivoting around 1.1365, USDJPY broke below 115.00 to new 10-day low at 114.78 back to 115.10 now. Cable breaches 1.3600 and trades at 1.3625.

Overnight – JPY hurt by weaker CPI data (0.2% vs 0.3% & 0.5% previously). Fed hawk Mester says rates should rise more quickly and the balance sheet needs to be reduced more swiftly than it did post the financial crash. Nothing new but more hawkish overtones and pressure to act. UK Retail Sales stronger than anticipated, 1.9% vs 1.1% but December numbers were revised down to -4.0% from -3.7%. Poor christmas for UK retailers. French CPI in-line and unchanged at 0.3%.

European Open – The March 10-year Bund future is down -13 ticks, US futures are also lower, but outperforming, with reports of a planned US-Russia meeting helping to boost confidence and boosting stock market sentiment. Safe haven demand is ebbing and DAX and FTSE 100 futures are up 0.3%, while a 0.7% rise in the NASDAQ is leading US futures higher. Not that Ukraine jitters are resolved and markets will keep a weary eye on developments. For now though they seem willing to buy into the headlines, which will likely see yields nudging higher early in the session. EGBs have staged a remarkable rally this week, as officials pledged caution and gradualism as they prepare to remove stimulus.

Today – US Existing Home Sales, EZ Consumer Confidence, Fed’s Williams, Brainard, Evans; ECB’s Elderson, Panetta. Earnings NatWest; Allianz, EDF, Deere.

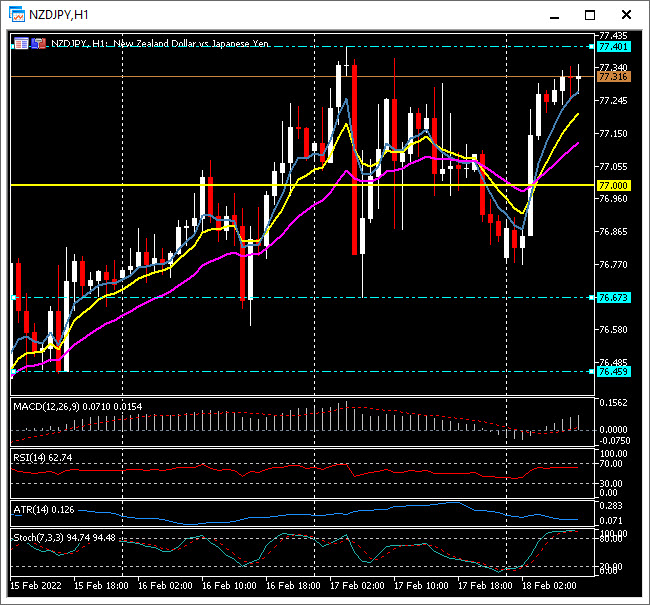

Biggest FX Mover @ (07:30 GMT) NZDJPY (+0.58%) Rallied from lows of 75.86 on Monday to 0.77.35 now. MAs aligned higher, MACD signal line & histogram significantly above 0 line, RSI 63.25 & rising, Stochs OB zone H1 ATR 0.123 Daily ATR 0.755.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.