Stock market sentiment started to stabilise overnight after Wall Street closed up from session lows. US futures are in the red though, led by a 0.8% drop in the USA100, and as officials in Europe and the US announce stiff sanctions for Russia, traders are also mulling what that means for Europe. Higher energy prices clearly are one thing and Brent is still holding above the $100 per barrel mark this morning. Russia’s oil exports seem to have been spared for now, while allies blocking access of the Swift payment system is also a possibility should a further escalation of sanctions become necessary.

- USD settled lower below 97.00 (USDIndex 96.86).

- China’s PBOC made a large liquidity injection. China’s central bank injected net 290 billion yuan via seven-day reverse repo operations today. That is the largest amount since September 2020 and according to the PBOC is designed to keep liquidity stable over the month end. The wild ride in global stock markets may have contributed to the move as external pressures, including the rise in oil prices, will add to existing problems, including the slump in the property markets and Covid related restrictions. The combination will likely keep the PBOC on an easing path.

- The VIX slid back to the 28.50 region after spiking to 37.79.

- US Yields – 10-year is down -0.3 bp at 1.96%, while the 10-year JGB rate has lifted 2.0 bp to 0.203% and yields are also higher in Australia and New Zealand.

- Equities – GER30 and UK100 futures are currently up 1.65% and 1.2%. JPN225 gained nearly 2% and the CSI 300 is currently up 0.8%. USA100 round tripped, bouncing 3.35% higher after tumbling -3.4%, while USA500 recovered to post a 1.59% gain from a -2.6% drop, with USA30 rising 0.28% versus a -2.6% morning drop.

- USOil – fell back to $89.60 lows after hitting 7-year highs of $100.50 ahead of the open. Currently at $93.70.

- Gold – tumbled from a $1974 high down to the $1885 area.

- Bitcoin back above PP at $37,700.

- FX markets – EURUSD at 1.1210 from 1.1110 low, USDJPY back above 115.15, Cable breached 1.3438.

European Open – Europe’s reliance on Russian oil and gas comes at a price and will be something officials need to address urgently, although there is of course no quick solution, which means consumers will feel the pain of even higher energy costs. The jump in the cost of living is already depressing consumer confidence, and after the disappointing German GfK consumer confidence reading earlier in the week, the UK’s numbers overnight looked equally depressing. The pressure on central bank to step in will remain then, even against the background of the crisis in Ukraine.

DATA: German Q4 GDP revised up markedly – to -0.3% q/q from -0.7% q/q reported initially. German import price inflation hit 26.9% y/y in January, another higher than expected number that is likely to explode in coming months when the jump in oil prices is reflected, as it seems extremely unlikely that oil prices will go down very quickly in light of Russia’s invasion of Ukraine. European gas prices exploded yesterday and are also likely to remain very high, which means more pain for consumers ahead, as the cost of living explodes.

Today – Today’s data calendar includes detailed German GDP, preliminary French inflation numbers, the Eurozone ESI confidence reading, US PCE, Durable Goods and Michigan index. EU and ECB officials are set to hold a presser today, likely detailing some sanctions against Russia and their implementation.

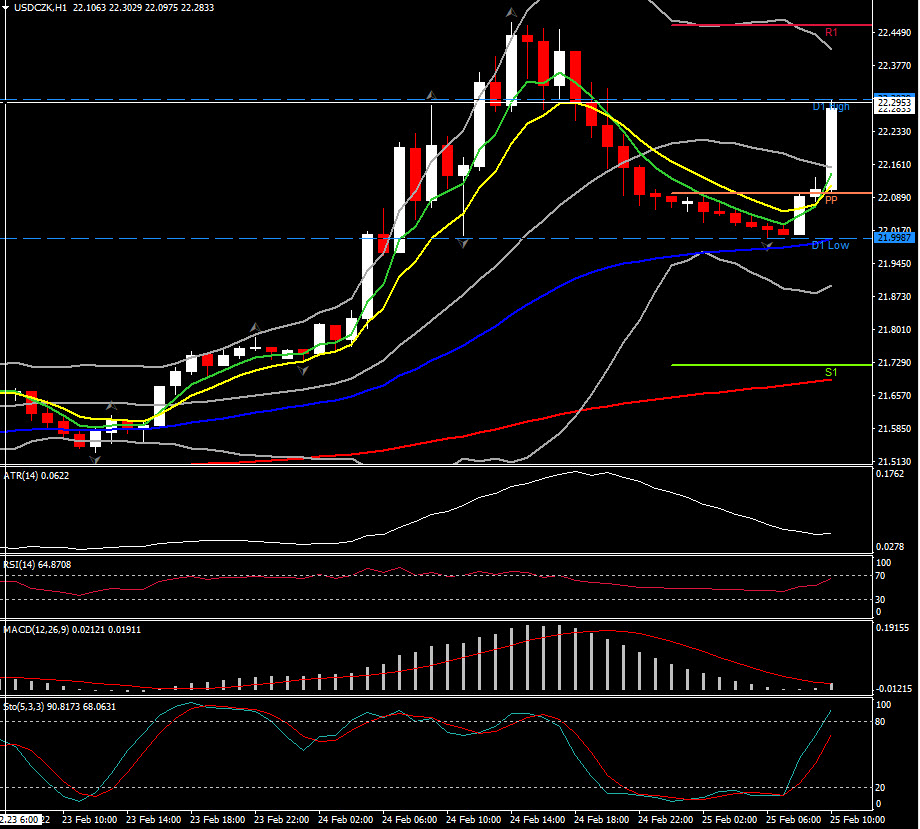

Biggest FX Mover @ (07:30 GMT) USDCZK (+1.18%) spiked to 22.30 from 21.99 on EU open. MAs bulishly crossed, MACD signal line & histogram remain close to 0 line, RSI 64 & rising. H1 ATR 0.0622, Daily ATR 0.2683.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.