Risk On re-emerged yesterday as stocks rallied (NASDAQ +3.59%, Nikkei +3.8%) as Russia-Ukraine Fin. Mins. meet in Turkey, OIL dived (-12% at one point) as UAE said it would increase output, but not break with OPEC. GOLD fell $85 & JPY & CHF dipped as safe haven assets fell (USDJPY over 116), USD slipped too, EUR had its best day in months (EURGBP back to 0.8400) ahead of ECB later. AUD & NZD hold their bid too. Yields fell and BTC stalled at key $42k level and lost over $2k. Overnight JPY PPI leapt to 9.3% due to significant imports.

- USD (USDIndex 98.04). Cooled from over 99.06 yesterday to 97.80 before recovering 98.00.

- US Yields 10-yr up to 1.948% on close – lower to 1.934% now. Yesterday’s 10-yr auction was filled at 1.92.

- Equities – USA500 +107 (+2.57%) 4277. US500 FUTS down at 4270 now. Tech rallied over +5% (Google, MSFT, NFLX & TWTR). XOM lost -5.6% as oil prices collapsed. Amazon +2.4% announced 20-for-1 stock split.

- USOil – Tanked from $124.90 highs on Tuesday to $99.70 yesterday. $107.50 now.

- Gold – Down from Tuesday high at $2070 to under $1975 now.

- Bitcoin tested the key $42K level yesterday, only to reverse under $40k & trades at $39,300 now.

- FX markets – EURUSD back over 1.1050, USDJPY holds over 116.00 and Cable up to 1.3190 now.

European Open – The June 10-year Bund future is up 15 ticks at 163.75, outperforming versus Treasury futures. Yields moved higher across Asia, but the broad reversal of safe haven flows that dominated yesterday’s session has already started to run out of steam, as doubts over hopes that Ukraine and Russia will come to an agreement at the scheduled meeting of foreign ministers in Turkey today have crept in. US futures are broadly lower, even if DAX and FTSE 100 futures are adding to yesterday’s gains. The correction in oil prices eases some of the recent pressure and for the Eurozone at least, while support also comes from hope that EU heads of state will agree to joint debt issuance to finance energy and defence policies in light of Russia’s invasion of Ukraine and the escalating tensions between the West and Russia.

ECB Preview – The ECB meets today and another joint debt package would increase the central bank’s room to extend net asset purchases, which most now expect the central bank to keep open ended at today’s meeting as warnings of stagflation fears dominate the headlines. Still, the ECB can’t afford to do nothing and may find a way to change strategy and open the way to hike rates, while still buying bonds.

Today – US CPI, ECB Policy Announcement & Press Conference (Lagarde), Weekly Claims, Russia-Ukraine Foreign Ministers in Turkey & EU Leaders Summit, RBA’s Lowe.

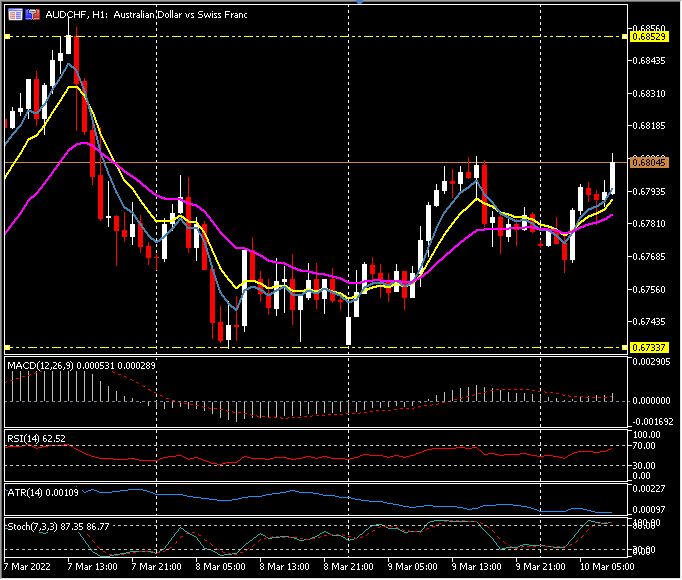

Biggest FX Mover @ (07:30 GMT) AUDCHF (+0.40%) Rallied from 0.6735 lows yesterday to over 0.68.00 now. MAs aligned higher, MACD signal line & histogram hold over 0 line, RSI 62 & rising, Stochs in OB zone. H1 ATR 0.0011, Daily ATR 0.0070.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.