US CPI is at a fresh 40-year peak, and there was a hawkish slant from the ECB for which the markets were not fully prepared. Risk off prevails with Asian stocks mostly sold off, after a largely weaker close on Wall Street. Japanese indexes underperformed and the Nikkei lost -2.1%, while the ASX was down -0.9% at the close. The Hang Seng corrected -1.6%, weighed down by tech stocks after the US flagged five Chinese firms that could be delisted. Oil dived to 101.25 amid escalating bans on Russian oil. President Biden will call for an end to normal trade relations with Russia. US & G7 allies to move today to strip Russia of ‘most favored nation’ status.

- USD (USDIndex 98.63) steady below 99.40 highs.

- US Yields 10-yr cheapened 6 bps to the 2.00% area. The 2-year rate was at 1.715%. The wi 30-year tested 2.40% prior to the sale but closed around 2.38%.

- Equities – USA100 closed with a -0.95% decline, while the USA500 and Dow were down -0.43% and -0.34%, respectively.

- USOil – dipped to $101.25 but up to $105.09 now. Set for its biggest weekly drop since November.

- Gold – lower as US Treasury yields gained overnight on red-hot inflation data. Currently at $1990.

- FX markets – EURUSD back below 1.1000, USDJPY at 5-year tops at 116.79 and Cable languishes at 1.3093 near a 16-month low.

European Open – Eurozone bond yields spiked and spreads widened in the wake of the ECB announcement yesterday, which confirmed the ECB’s path to policy normalisation. Net asset purchases are set to be scaled back through the second quarter and likely to end in Q3, and while that paves the way for rate hikes in Q4, the ECB made it clear that rate moves will depend on geopolitical developments. The Ukraine war has left the growth outlook with clear risks to the downside and the inflation outlook with considerable upside risks, which complicates the matter, but it is clear that for now the ECB remains determined to phase out stimulus as inflation is unlikely to undershoot the target in the medium term.

Overnight: Japanese real spending dropped -1.2% in January, following the 0.2% bounce in December. German February HICP inflation was confirmed at 5.5% y/y, rising from 5.1% y/y in the previous month. UK monthly GDP was stronger than anticipated. The economy expanded 0.8% m/m in January.

Today – With the focus firmly on the Ukraine war, data releases continue to take a back seat, but for what it is worth, today brings Canadian Labor data.

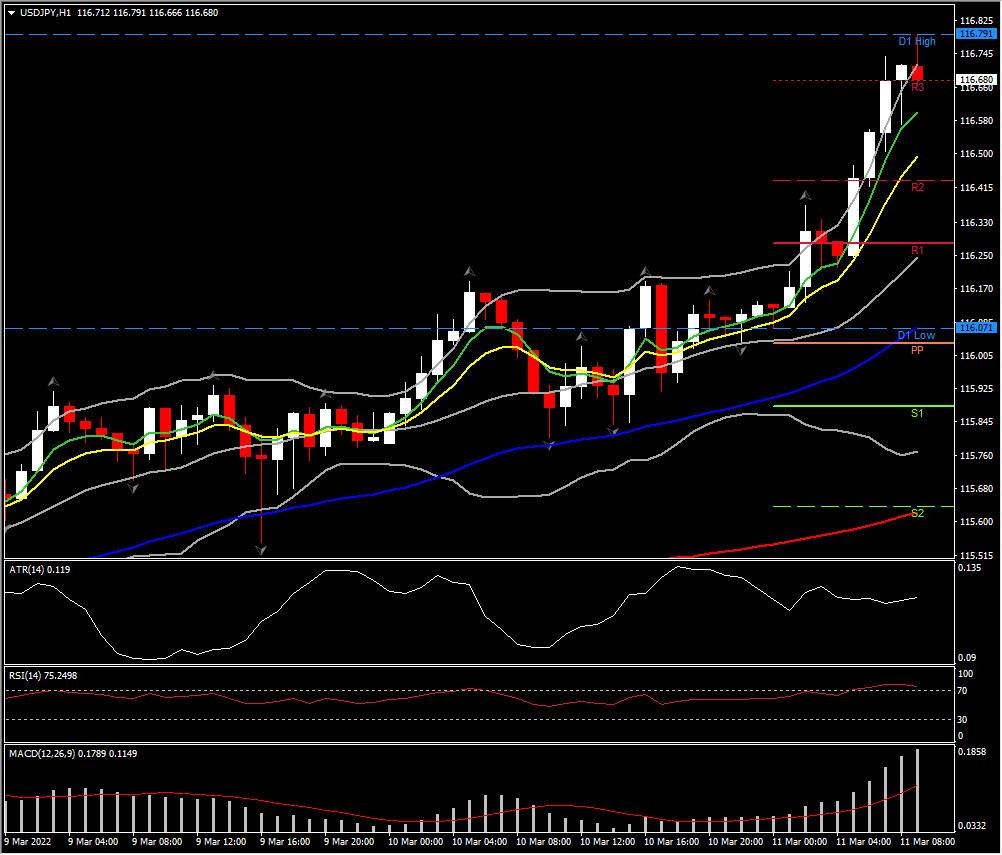

Biggest FX Mover @ (07:30 GMT) USDJPY (+0.51%) Rallied to January 2017 highs at 116.79. MAs pointing right, MACD signal line & histogram hold well above 0 line, RSI 76 & flat, all implying near term consolidation but overall strong positive bias.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.