The Ukraine war remains in focus, but the FOMC announcement and the BoE decision are also coming into view. Russia’s attack on Ukraine seemed to intensify over the weekend, with bombs falling near the Polish border. US reports that Russia has asked China for military assistance also flagged the risk of a further escalation of the war, but at the same time there were some hopes of diplomatic progress ahead of fresh talks.

- USD (USDIndex 99.05) strong, helped by speculation that the spike in commodity prices will push the FOMC into an aggressive tightening cycle.

- US Yields 10-yr jumped 4.6 bp to 2.037%, amid speculation that the spike in commodity prices will push the Fed into an aggressive rate hike cycle. The June 10-year Bund future is slightly lower, but outperforming versus US futures, which have sold off.

- Equities – GER30 and UK100 are up 1.1% and 0.6% respectively, with US futures also higher. USA100 closed with a -0.95% decline, while the USA500 and Dow were down -0.43% and -0.34%, respectively. Nike and Apple weighed on the blue chips, while all 11 S&P sectors were in the red. Communications services and technology lagged, both down 1.8%, while utilities outperformed, about 0.4% lower.

- Reuters: China, the world’s largest crude oil importer and second largest consumer after the United States, is seeing a surge in COVID-19 cases, as the highly transmissible Omicron variant spreads to more cities, triggering outbreaks from Shanghai to Shenzhen.

- USOil – shed to $103.50 and consolidating as diplomatic efforts to end the war in Ukraine geared up and markets braced for higher US interest rates.

- Gold – lower at $1971 ahead of FED.

- FX markets – EURUSD is consolidating above the 1.09 mark amid lingering hopes that diplomatic efforts can prevent a further escalation of the war in Ukraine, USDJPY rising to levels last seen in 2017, with the pair currently trading at 117.83 and Cable languishes at 1.3018. The Yen struggled, and even more so AUD overnight.

Fed policy outlook: the FOMC meets (Tuesday, Wednesday) and this will be an important meeting, even though it will be overshadowed by the Ukraine war and the extreme volatile and uncertainties in the markets. What the latter have done, however, is temper any potential aggressive action from the Fed and other central banks as policymakers look to address decades high, if not record inflation, while not driving growth into the ground. Along with the universally expected 25 bp hike, versus the 50 bps or even 75 bp a few weeks ago, new quarterly projections will also be released. These forecasts will be subject to tremendous uncertainty, but we see big downward revisions to 2022 GDP growth and huge upside boosts to PCE chain prices estimates.

Today – The FOMC announcement on Wednesday is already casting its shadow. The BoE is due Thursday and also expected to hike rates again, after the better-than-expected GDP report from last week and with officials noting upside surprises in wage growth. Official UK labour market data is due tomorrow, but for today, the European calendar is relatively quiet.

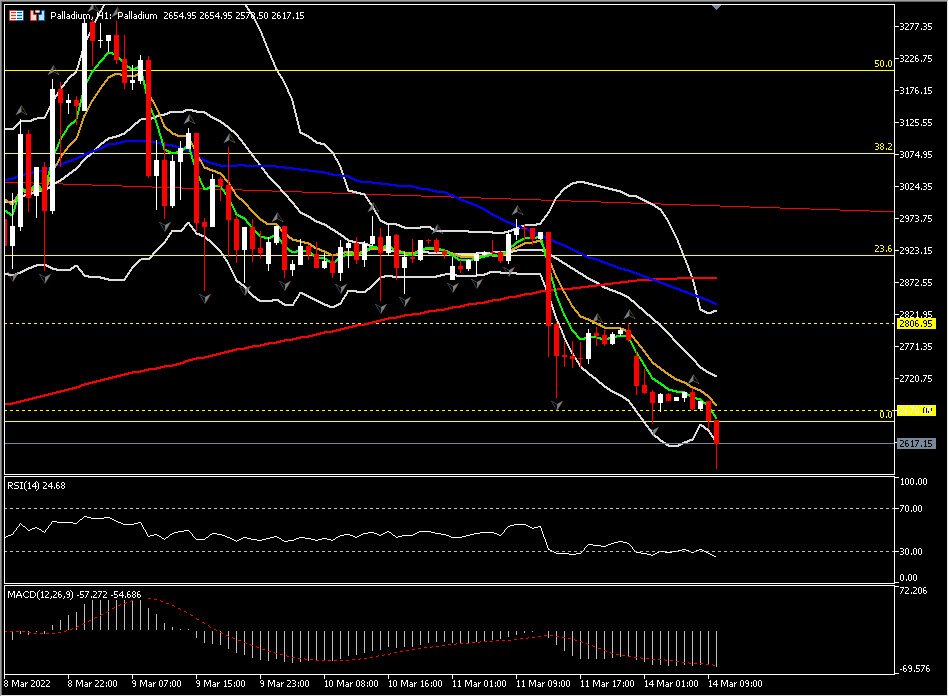

Biggest FX Mover @ (07:30 GMT) Palladium (-6.33%) Dipped to 2578. MAs pointing down, MACD signal line & histogram hold well above 0 line, RSI 23 & falling, all implying negative bias.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.