Risk aversion continues to dominate as Russia’s attack intensifies and hopes of resolution through talks fade. Stagflation concerns and the longer term impact on the recovery are keeping a lid on stock markets and complicating the outlook for central banks. The BoE managed to pull off a “dovish rate hike” last week, China’s central bank kept lending rate unchanged in line with expectations, while SNB is expected to keep policy settings on hold this week. At the same time, China’s lockdown in the tech hub of Shenzhen threatens to lead to ongoing delays in long awaited deliveries. German PPI inflation hit 25.9% y/y in February – sharp rise in cost pressures even before the impact of the Ukraine war had really taken hold. Energy price inflation hit 68.0% y/y. No surprise that many at the ECB are getting nervous, especially as the risk of rising wage pressures is mounting.

- USD steady (USDIndex 98.30)

- Equities – After PBOC, Asian shares were down. ASX was down -0.2% at the close, while Hang Seng and CSI 300 are currently posting losses of -0.9% and -0.2% respectively. US futures are also in the red, after the strongest week since November 2020. GER40 and UK100 futures are down -0.2% and -0.02% respectively.

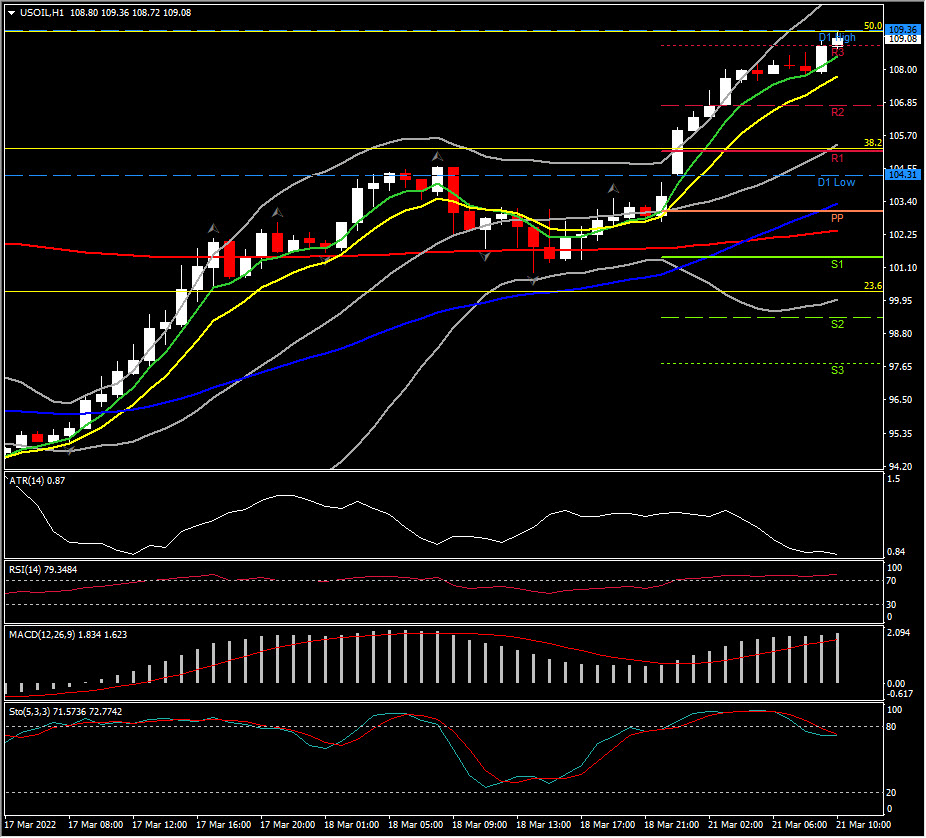

- USOil – Rallied to $108.80 – attacks by Iran-backed rebels on energy facilities in Saudi Arabia pushed up prices.

- Gold – remains under pressure at $1925.

- Bitcoin holds the break of $40,000 yesterday, trades at $41,055 now.

- FX markets – EURUSD back to 1.1050, unable to hold breach of 1.1100, USDJPY at 119.20 and Cable pullback to 1.3155.

Today – There are a number of ECB and BoE speakers scheduled this week that could attract attention in nervous markets. PMI reports in particular will be in focus in light of Ukraine tensions and the pick up in energy prices.

Biggest FX Mover @ (07:30 GMT) USOIL (+4.03%) Rally continues to 109.36, reversing 50% of March losses. Fast MAs aligned higher, MACD signal line & histogram strong, RSI 79 and rising, H1 ATR 0.87, Daily ATR 9.25.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.