The surge in Treasury yields was the story of Monday’s trading after Fed Chair Powell underscored the hawkish stance coming out of the FOMC meeting. The reaction in bonds showed a lot of jitters over the outlook and the ability of the Fed to achieve a soft landing. The US curve flattened markedly yesterday as the short end underperformed amid concern the Fed will hike rates aggressively. Stock market sentiment still looked much better across Asia than in Europe and even the US. The US Dollar was sought as oil prices lifted with WTI currently trading at $114.90. Energy prices are on the rise again and central banks are set to rein in stimulus with ECB’s Rehn yesterday confirming that in the central scenario the ECB is eyeing a lift off in rates for Q4 or maybe Q1 next year. Wall Street was depressed in choppy action, correcting from the prior week’s healthy gains as the FOMC looks to rein in demand to help address the inflation pop, which now looks to be longer lasting and more widespread due to the supply shock from the Ukraine war.

- USD up (USDIndex 98.94).

- 10-year Treasury rate is up 4.7 bp, the 2-year 7.0 bp, June 10-year Bund future is down 70 ticks, US futures are down -12 ticks. The JGB rate has lifted 1.1 bp and rates in Australia and New Zealand jumped 14.0 bp and 13.0 bp respectively in catch up trade.

- Equities – Nikkei lifted 1.5%, ASX lifted 0.86%, and the Hang Seng jumped 2.1%, even as US futures declined. Hong Kong was boosted by Alibaba Group Holding Ltd’s $25 bln share buyback program and by contrast, the CSI 300 is currently slightly in the red. The USA30 slid -0.58%, with the USA100 sliding -0.4%, while the USA500 was off -0.04%.

- USOil – renewed rise in oil prices, to $112.22 – currently lower to 108.68.

- Gold – remains under pressure at $1934.

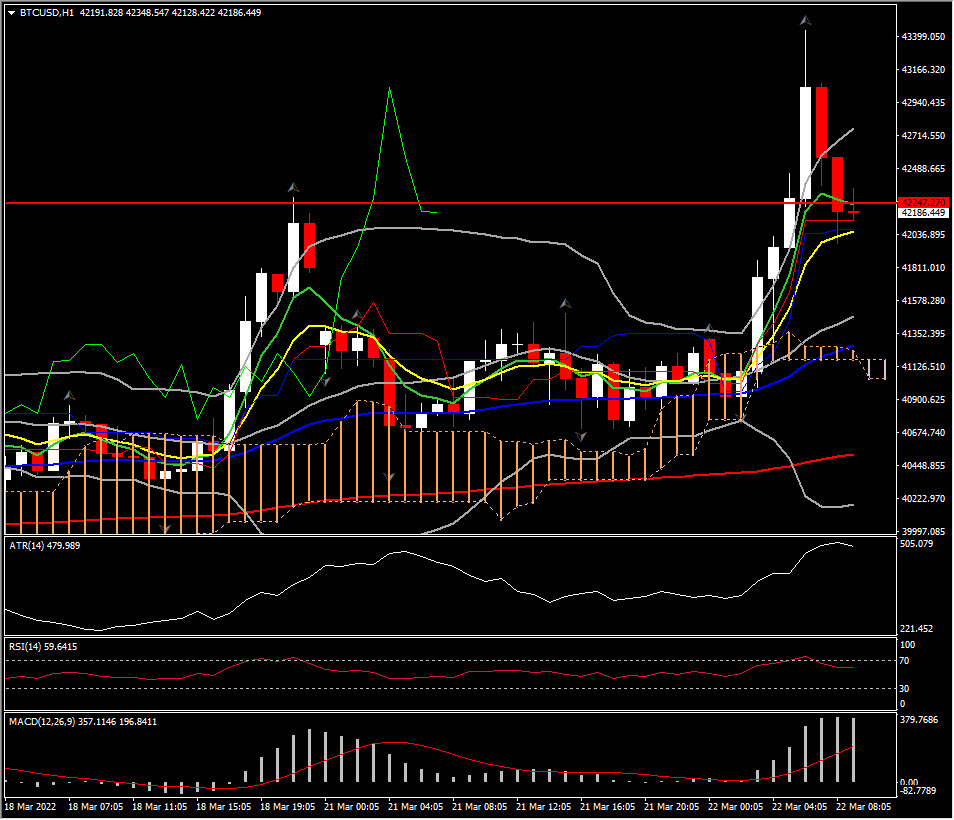

- Bitcoin breaches the $43,400, trades at $42,185 now.

- FX markets – EURUSD dips to 1.0960, USDJPY climbed to 120.48 and Cable rallied to 1.3136.

Today – UK public finance data and even more so the presentation of the budget will be of interest also for markets. The calendar today has Eurozone current account data, which is unlikely to attract too much attention.

Biggest FX Mover @ (07:30 GMT) BTCUSD (+2.63%) Rally continues to 43,437, breaking the top of March 18. Fast MAs flattened along with RSI (59) but MACD signal line & histogram remain strong, implying near term pullback. H1 ATR 479.989, Daily ATR 2405.790.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.