USD holds gains (USDJPY broke 125.00) and Treasury market fell again with US Treasury 5-to-30-yr yield curve remaining inverted suggesting economic slowdown & possible recession. US 10-yr slips back under 2.5%. Oil markets slumped (-1.0%) again on worries from Shanghai lockdown. US stocks rallied (NASDAQ +1.71%) growth stocks (TESLA +8%) gained as Banks & Energy stocks (Exxon -2.81%) fell. Asian markets higher (Nikkei & ASX +0.8%) except Chinese stocks.

BoE’s Bailey warned of a worse energy crisis than in the 70s, & highlighted that the BoE had already softened its rate guidance, even as it hiked rates again and flagged the chance of further tightening. Russian & Ukrainian negotiators meet in Istanbul later today. Limited expectations. Israel/Arab summit talked of united front to confront Iran. Biden proposed $5.79 trillion budget for next year increasing spending on Defence & raising taxes on wealthy. UK Met. Police to issue “Partygate” fines “imminently”.

Overnight – AUD Retail Sales better than expected (1.8% vs 0.9% & 1.8%)) & JPY Unemployment better (2.7% vs 2.8% & 2.8%) German GfK Consumer confidence missed -15.5 vs -14.6 & -8.1 last time).

- USD (USDIndex 99.00). Rallied to top at 99.35 yesterday.

- US Yields 10-yr up to 2.53% new 3-yr highs yesterday, now down to 2.483%

- Equities – USA500 +32.01 (+0.71%) 4575. US500 FUTS now at 4572 now. TSLA suggested another stock split and rallied over 8.0%, AMC up over +45% as the meme stocks raised their heads again.

- USOil – Fell again (over 1.1%) to $102.80 yesterday, but has recovered $105.00.

- Gold – slipped to $1916 yesterday from Friday’s close $1955. Back to $1922 now.

- Bitcoin holds onto gains over 45K to top at 48.1K, yesterday, back to 47.5k now.

- FX markets – EURUSD back to test 1.1000, now after 1.0950 test yesterday, USDJPY over 125.00 & new 7-yr highs back to 123.40 now as JP Government signals worries over weak Yen. Cable back to 1.3066 yesterday, recovered 1.3100 now.

European Open – The June 10-year Bund future is down 33 ticks, while in cash markets the 2-year Treasury yield is up 2.8 bp. Curve flattening continues as markets fret about the risk that aggressive central bank action will sap demand. DAX and FTSE 100 futures are up 0.9% and 0.6% respectively, US futures are also slightly higher, after a largely positive session across Asia, with hopes of progress in scheduled peace talks between Russia and Ukraine this week helping to underpin confidence.

Today – US JOLTS, CB Consumer Confidence & Case-Schiller Housing Index. Speeches from Fed’s Williams, Bostic & Harker, ECB’s Kazimir. EARNINGS – Micron & Lululemon.

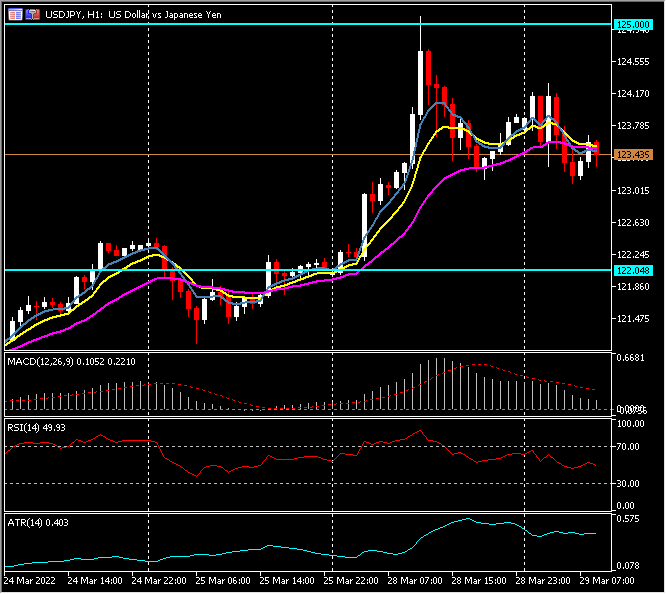

Biggest FX Mover @ (07:30 GMT) USDJPY (-0.34%) BOJ & Japanese Government raise concerns over weak Yen, following break of 125.00. MAs turned lower, MACD signal line & histogram now cooling, RSI 49.55, OB but rising, H1 ATR 0.403, Daily ATR 1.123.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.