- USD & Treasury yields have been rising. Stock markets have been under pressure, hit by the surge in yields with the tech-heavy index (USA100) plunging -2.26% as selling picked up into the close.

- The market has priced in a lot of bearish elements, yields shot higher again on hawkish comments from Fed, RBA. Disappointing China PMI reports weighed on both bond and stock market sentiment.

- USOil up to $102.48 as West mulls further sanctions against Russia. – Saudi boosted prices by over by $2 per barrel in late March.

- US coal prices climbed over $100 a ton today for the first time in 13 years after the EU said it is mulling restricting coal imports from Russia.

- US Rates on the 5-, 7-, and 10-year maturities were up almost 17 bps to 2.7108%, 2.678%, and 2.565%, respectively. The bond was 13.5 bps higher at 2.596%, while the 2-year rose over 10 bps to 2.526%. The bear curve steepened to 4.8 bps, after having been inverted for the prior three sessions at -3 bps Monday and -8 bps Friday.

- USD (USDIndex 99.72) rallied from 98.80 yesterday.

- Equities – USA500 -72.15 (1.57%) at 4530. US500 FUTS 4547. Banks & Technology stocks led the broadbased month end decline.

- Gold – steady at $1920 low after 1947 high yesterday.

- Bitcoin closing the gap at 45370?

- FX markets – EURUSD dipped to 1.0883, USDJPY continued to struggle at 124.04, Cable back to 1.3120 now. AUD and NZD also remained supported as yields moved higher.

European Open – The German manufacturing orders came in much weaker than expected, with orders falling -2.2% m/m in February. The actual slump was a surprise that will add to concerns that the German manufacturing sector could be heading for recession as the spike in energy prices and supply chain disruptions hit Germany’s industrial core. Exports orders dropped -3.3% in February.

FOMC preview: The minutes should prove very interesting to the markets as they should provide details on the balance sheet run off. We’ll also read the various comments about the abrupt, hawkish pivot from the FOMC, although we already know that the threat of surging inflation and the likelihood that it would not prove as “transitory” as expected, along with the robust recovery and strength in the labor market, were the major factors that finally forced the Fed to shift into high gear by accelerating the pace of trimming accommodation and then eye aggressive rate hikes. The dot plot reflected the pivot, and Fedspeak since then has affirmed it. Governor Brainard’s comments Tuesday, in fact, indicated the Fed would announce the start of balance sheet reduction as soon as May. She also supported her colleagues’ views on the need for a larger and speedier pace of balance sheet runoff. We will look for details on that in the minutes. We suspect at a minimum the Fed will double the pace of that from the last cycle with $60 bln in Treasuries and $30 bln in MBS, although the still hot housing market could see a higher cap on MBS.

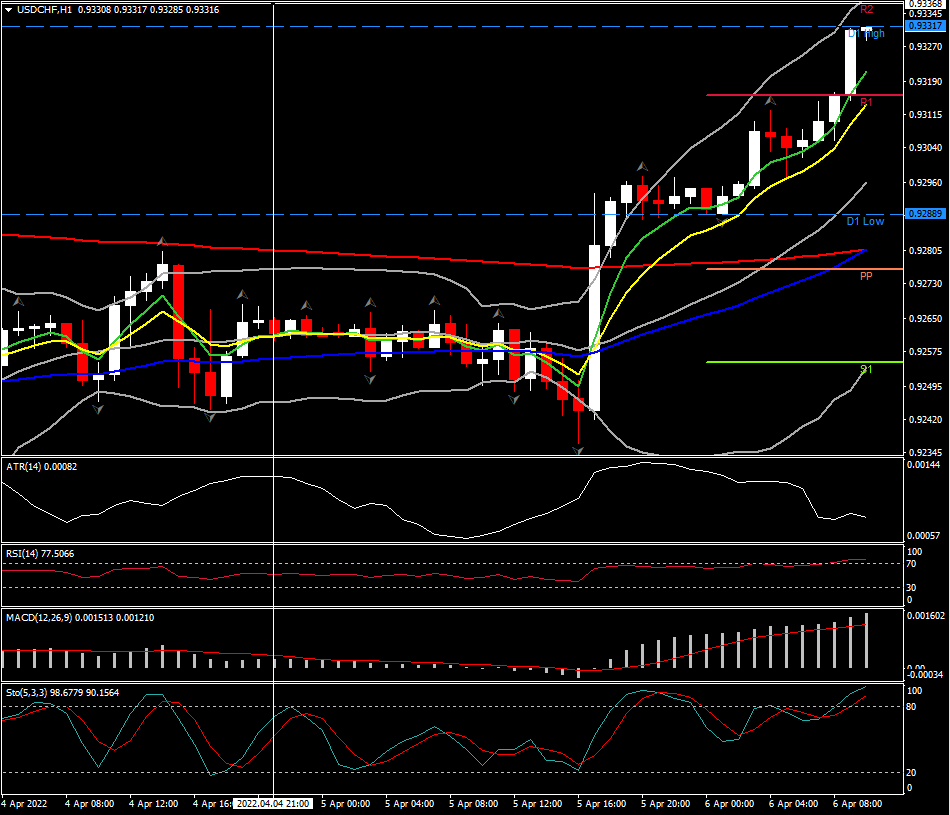

Biggest FX Mover @ (07:30 GMT) USDCHF (+0.37%) At 6-day highs and close to R2 at 0.9331. Next resistance 0.9376. MAs aligned higher, MACD signal line & histogram higher & over 0 line, RSI 77 & rising, H1 ATR 0.00087, Daily ATR 0.00617.

Click here to access our Economic Calendar

Andria Pichidi

Μarket Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.