Yields remain bid, supporting USD as Stocks sink. JPY & EUR remain weak. Oil recovers, Gold holds gains. –

- Stocks tanked (NASDAQ worst again -2.18%) Weak in Asia (Nikkei -1.72%) & UK & European FUTS. lower (0.2 to 0.6%).

- Yields rally as curve steepens – US 10-yr now at 2.824%.

- EUR fell again after minor rally following French Election result. USD bid elsewhere.

- USD bid especially vs. weaker JPY (over 125.50 ), AUD, CAD & NZD.

- Oil recovered from key support, up over $4/barrel as Shanghai eases some lockdowns.

Biden told Modi that buying Russian oil is not in India’s “interest” & will help. Macron & Le Pen go on Election Blitz, Morrisson kicks off Australian Election campaign. Austrian PM meets Putin for 90 mins. New populist PM in Pakistan raises the min. wage. Zelenskiy says tens of thousands have died in Mariupol.

Overnight – JPY PPI inflation beats – 9.5% vs. 9.2% & 9.7% previously. In line UK Wages & Unemployment with Claims lower. AUD big boost for Business Confidence (16 vs 13) and German HICP at 7.6%, levels last seen in the early 1980s.

- USDIndex rallied to test new high 100.17 , trades at 100.12 now.

- US Yields 10-yr closed higher again at 2.78, up again now to 2.824%.

- Equities – USA500 -75.75 (-1.69%) at 4412. – US500 FUTS 4393. Technology stocks & Consumer Discretionary led decline, TSLA -4.85%, NVDA -5.2% AT&T +7.46%

- USOil – Trades at $97.30 following a dip to $93.00, Shanghai eases some lockdowns.

- Gold – gyrated from $1969 to $1940, yesterday , back to $1958 now.

- Bitcoin continued to decline from key 45k to trade at 39.88k now.

- FX markets – EURUSD back to test 1.0860 now from 1.0935 yesterday. USDJPY breaks key 125.50 to trade at 125.75 and Cable sinks back to test 1.3010 as USD bid continues.

European Open – The German 10-year Bund yield is up 1.5 bp at 0.82%, the 10-year Gilt rate has lifted 1.7 bp at1.86% in opening trade, alongside a 3.3 bp rise in the U.S. Treasury yield. Eurozone spreads, which narrowed yesterday, are mostly wider this morning, especially at the short end, and the US curve has flattened slightly, as the short end underperforms ahead of key US inflation data. Markets are nervous that a higher than expected figure could prompt the Fed to head for an even more aggressive tightening cycle than currently expected and in Europe, the high German inflation reading is putting pressure on the ECB ahead of Thursday’s meeting.

Today – US CPI, (1.2% m/m 8.4% y/y) – but watch the CORE figures for any sign of actual weakness. Speeches from Fed’s Barkin & Brainard.

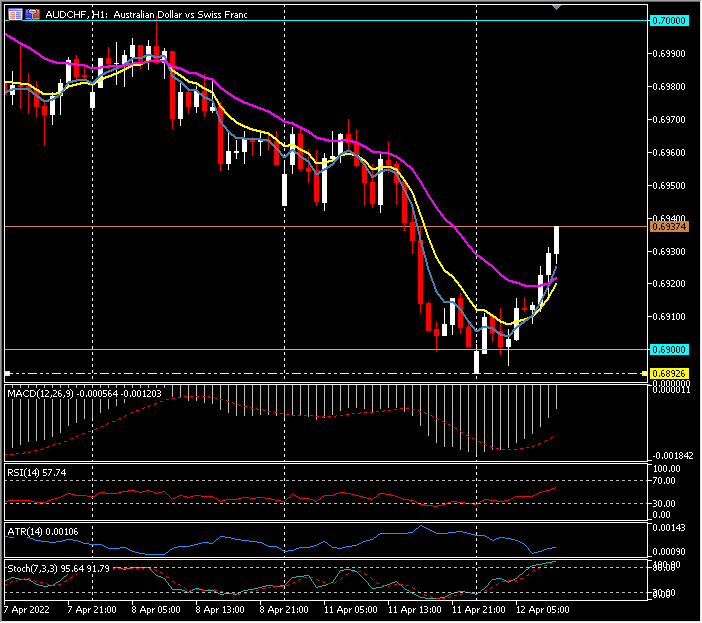

Biggest FX Mover @ (07:30 GMT) AUDCHF (+0.47%) Recovering from 4-day decline to below 0.6900 at 0.6893 earlier to 0.6935 now. Next resistance 0.6950 & 0.6970. MAs aligned higher, MACD signal line & histogram moving higher but below 0, RSI 56.50 & rising, H1 ATR 0.00105, Daily ATR 0.00685.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.