Last week was dominated by volatility as the RBA, FED and BOE gave the markets something to think about. Accelerating global price pressures following the pandemic have left central bankers with the tough tradeoffs between inflation and growth, as each dynamic has debilitating consequences for global economies, and policymakers are trying to walk a fine line between the two. The FOMC is prioritizing the inflation fight as the strength in the labor market suggests little chance of a sustained US downturn. The RBA hiked rates more than expected, the Fed took a possible 75 bps hike off the table and the BOE said not to look for too many rate hikes, while raising inflation forecasts and calling for a possible economic contraction in Q4.

Across the pond, it is becoming a major battle between the doves and hawks at the BOE and ECB as the war, sanctions, and supply chain disruptions are significantly increasing risks to growth while inflation is going through the roof. And in Asia, the zero-covid policies and restrictions in China are exacerbating a worrisome slowing in activity while price pressures are relatively tame. Inflation and growth reports will be the highlights ahead.

RBA surprised markets by raising interest rates for the first time since 2010, by 25 bps from 0.1% to 0.35%. The committee suggested there could be more gains in the future, as inflation picked up faster than anticipated. The AUDUSD picked up quickly, but was also quickly sold off in the last week, as fears of slowing growth in China following Covid-19 lockdowns affected the Australian Dollar.

China’s trade data for April released earlier this morning showed imports exploded last month, as tighter lockdowns of major cities and worse prints are expected this month, with imports set to fall -3% on the yearly measure. China’s annual inflation rate rose to a 3-month high of 1.5% in March 2022 from 0.9% in the previous two months and above market forecasts of 1.2%. China set its target CPI around 3% for the year, the same as in 2021. On a monthly basis, consumer prices were unexpectedly flat in March, compared to a consensus 0.1% decline and after a 0.6% gain in February.

This is bad news for countries that depend on China’s demand for their commodity products, especially Australia. With China’s economy slowing down dramatically, there will definitely be some negative effects on the Australian economy.

On the other side of the world, US inflation releases are the focal point this week now that the May policy meeting and the jobs report are out of the way. That pressures failed to abate last year and into 2022 as the FOMC expected has cost policymakers some credibility as the long-touted “transitory” inflation never materialized. The acceleration in prices to multi-decade, if not record highs by some measures, stirred fears the Fed was behind the curve and forced the Committee to aggressively increase interest rates — last week’s 50 bps hike was the largest since 2000.

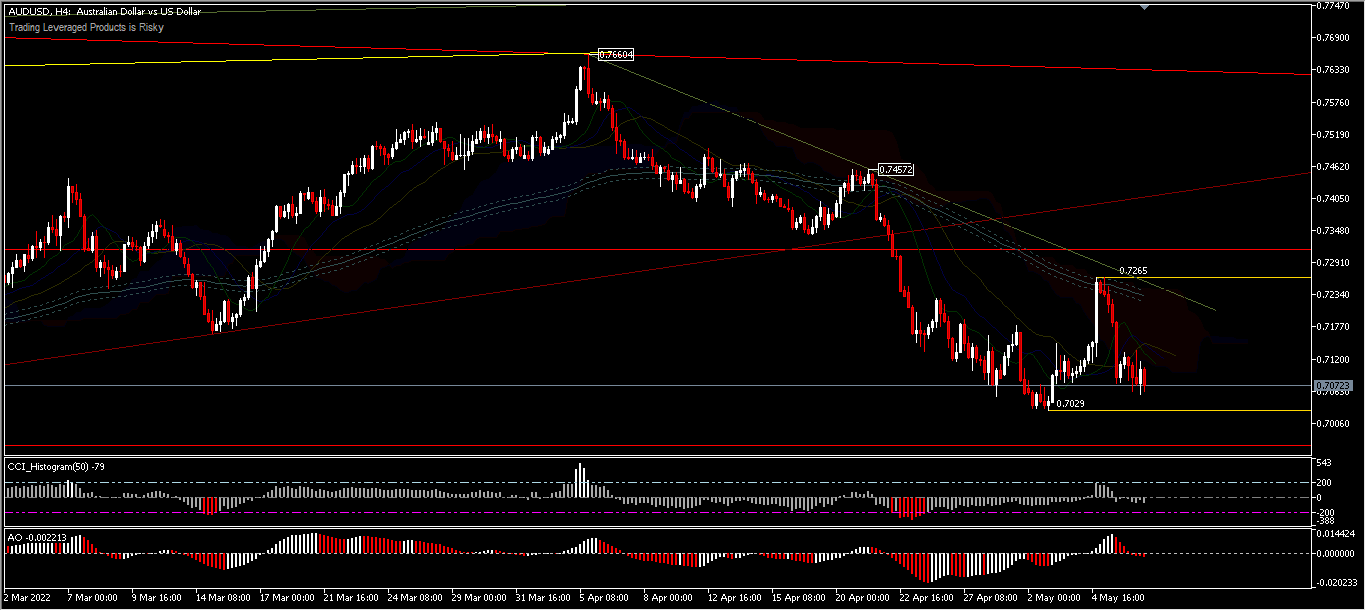

AUDUSD closed last week with a decline of -0.53% and closed at 0.7072. A move to the downside is possible to retest the 0.6966 low, as long as the 0.7265 resistance holds. A sustained break of the 0.6966 support will deepen the correction wave 0.8006 to the 50.0% FR retracement level in the 0.6775 price range in the coming weeks. Conversely, if the support at 0.6966 holds, it will take the asset into consolidation.

AUDUSD,H4– edged lower to 0.7029 last week, rebounding to 0.7265 before turning lower. The initial bias remains neutral this week and views are changing, that the decline from 0.7660 is the third move of the corrective pattern from 0.8006. A price move below 0.7029 will target the 0.6966 low first. A strong break there would confirm a medium term bearish case. However, a move above the price of 0.7265 will confuse the prospects for the future.

Technical indicators are still validating movement to the downside, with 2 oscillation indicators in the sell zone and price movement below the Alligator, Kumo and 200-period EMA.

New Zealand Dollar

Meanwhile, New Zealand’s strong labor market in Q1 and the unemployment rate at a record low of 3.2% brought no significant changes for the Kiwi, last week. The emergence of global growth concerns, especially in China, built a stigma for falling commodity prices which ultimately affected the New Zealand Dollar as a commodity currency.

NZ inflation hit 6.9% in Q1 and the RBNZ is determined to curb inflation expectations. The RBNZ raised interest rates by 0.50% in April to 1.50% and indicated further tightening is needed. Despite the RBNZ’s hawkish stance, the New Zealand Dollar underperformed amid the strengthening US Dollar.

NZDUSD continued its decline for the 6th week in a row, losing more than -6% in April and additional losses for May above -1%. The 0.6380 minor support looks soft, after the break of the 0.6528 support 2 weeks ago. Further declines should target the 61.8% FR retracement level around the 0.6227 price level. As long as the resistance at 0.6567 holds, the outlook remains bearish.

NZDUSD, H8

NZDUSD, H8

The intraday bias remains tilted to the downside for the FE100.0% projection at 0.6344 from a drawdown of 0.7217-0.6528 and 0.7033. However a move above the 0.6567 resistance would confuse the short-term outlook. Technical indicators are still validating intraday price moves to the downside, overall.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.