Concern over Europe’s gas shortages remain in focus as the energy standoff with Russia intensifies. Aggressive central bank action and the prospect of further rate hikes meanwhile have kept a lid on Gold prices, while agricultural commodity prices remain at elevated levels.

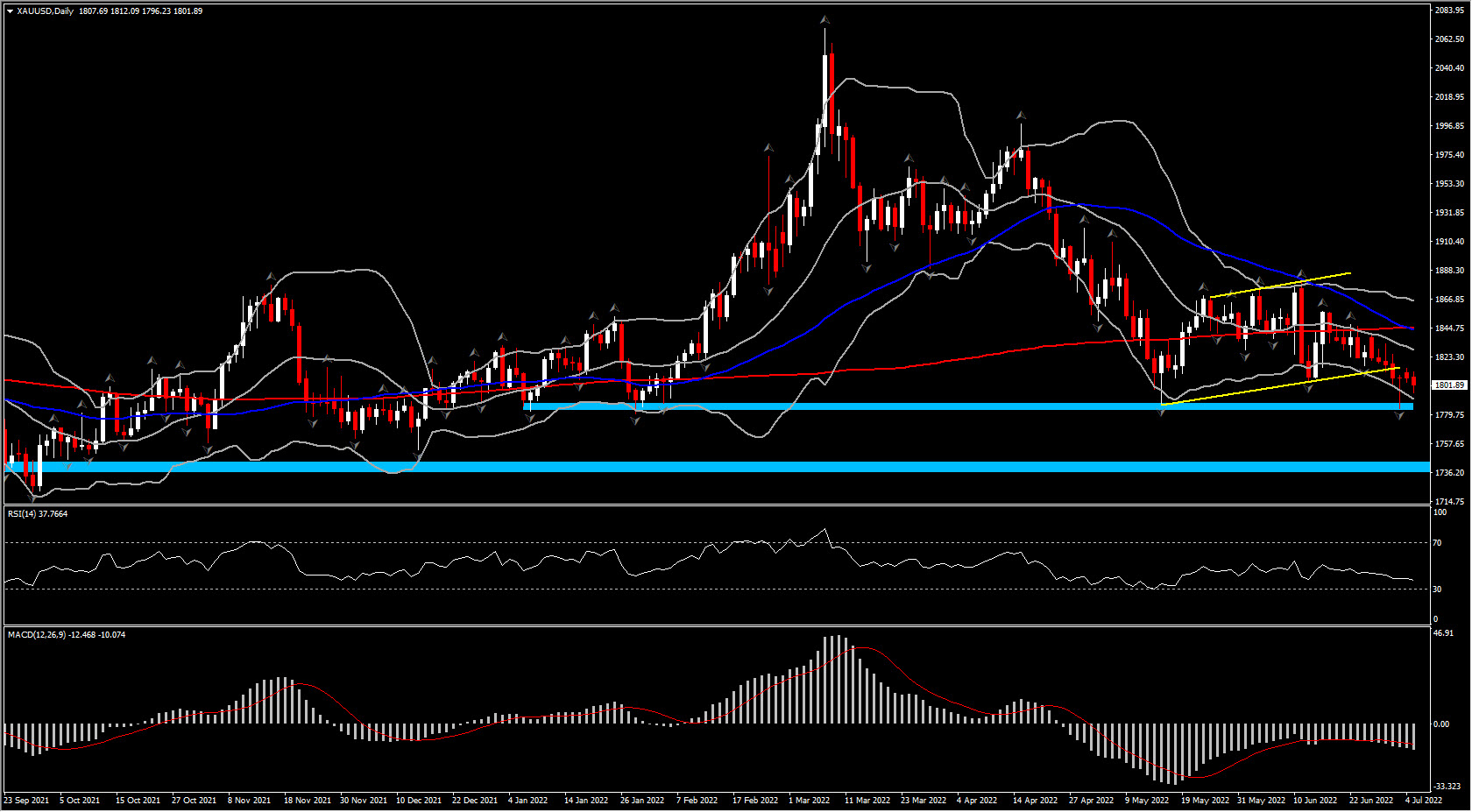

Gold prices have remained under pressure over the past week. Bullion declined for a third month running in June and briefly dropped below the $1,800 mark on Friday.

Gold prices are down on the day and seem to be preparing for another test of the USD 1800 mark. Bullion saw a low of 1780 as Treasury yields move higher and recession fears mount. Treasuries have recovered into the green with yields richer across the board. Haven demand is adding to gains in Treasuries and the US Dollar. The USDIndex has soared to 106.32, a fresh 20-year high.

The Atlanta Fed’s downward revision to Q2 GDP last week to -2% from -1% has added to worries over the U.S. economy. The belly of the curve is leading the gains with the 5-year yield over 5 bps richer at 2.82%. The 10-year yield is also off 5.3 bps at 2.827%. The 2-year is fractionally lower at 2.827%. The curve is flat but has flirted with inversion. That too will exacerbate recession concerns. The major Wall Street indexes are all down more than -1%.

The US Dollar is once again the main beneficiary of haven flows, with bullion struggling in the stagflation environment. With many still expecting another 75 basis point hike from the Fed, non-interest bearing gold is unlikely to make much headway at the moment. Indeed, recession fears may be picking up, but the Dollar rather than bullion has been the main beneficiary of haven flows in recent weeks.

USOIL has dropped back to $105.60 from session highs as recession fears mount and weigh on stock market sentiment. UKOIL is at $109.40 per barrel, as traders weigh recession concerns and supply disruptions. Unrest in Libya and a planned strike by Norwegian energy workers added to jitters today and longer term supply concerns are likely to keep prices trending higher.

OPEC+ countries last week signed off on the scheduled output increase for August, which in theory means all output cuts agreed to during the pandemic will be removed by then. The decision raised the combined production limit of the 20 members that have agreed targets to 648,000 barrels a day. However, while supply has been restored on paper, in reality actual production has not met these targets and combined output by the 20 countries fell more than 2.6 million barrels a day short of their goal in May, according to OPEC data. Only two members are likely to have significant spare capacity and the more consequential production decisions are expected to coincide with US President Biden’s visit to Saudi Arabia in August. The country is still expected to run down spare capacity ahead of the European embargo on seaborne Russian oil imports at the end of the year.

Meanwhile the G7 proposed a cap on Russian oil prices, which they hope to enforce via a ban on all services that enable Russian crude transports by sea. About 90% of the world’s marine protection and indemnity insurance is provided by the International Group of P&I Clubs, which comprise European, American and Japanese companies. There are still many details to be hammered out, but in theory the cap could work even without the explicit cooperation of India and China, which have been keen to take up some of Russia’s oil exports. Still, there is a substantial risk that the move will prompt Russia to retaliate by withholding energy exports.

German Economy Minister Habeck warned over the weekend that the country must prepare for possible cuts to gas supplies, while accusing Russia of “economic warfare” against Europe. The sharp hike in energy prices and rate hikes from central banks are likely to weigh on demand, but politicians are increasingly also concerned about the possible political fallout and the risk of social unrest against the threat of rationing over the winter months.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.