Oil prices have backed up further after the IEA increased its outlook for oil demand in the second half of the year and 2023 while saying Russian oil output, which didn’t correct as much as expected following the sanctions of the west, will drop a further 20% when the EU ban takes full effect next year. The USOIL lifted in the wake of the cooler than expected US inflation report yesterday, which dampened concerns that aggressive central bank action will translate into recession and curtailed oil demand.

IEA lifts demand forecast substantially. IEA said record European prices for natural gas are spurring “substantial” gas to oil switching and has lifted its demand forecast for 2022 by 380K barrels a day. “These extraordinary gains, overwhelmingly concentrated in the Middle East and Europe, mask relative weakness in other sectors, but will propel demand higher by 2.1m to 99.7m in 2022 and a further 2.1m b/d to 101.8m in 2023. The IEA also said the impact of western sanctions on Russian oil exports had been less severe than it had previously forecast, also thanks to the rerouting of flows to other countries, including India, China and Turkey. The embargo is likely to result in further declines after it comes into full effect in February 2023, but a “possible softening of measures”, still prompted the IEA to lift the production forecast for Russia by 500K a day in the second half of this year and by 800K for 2023.

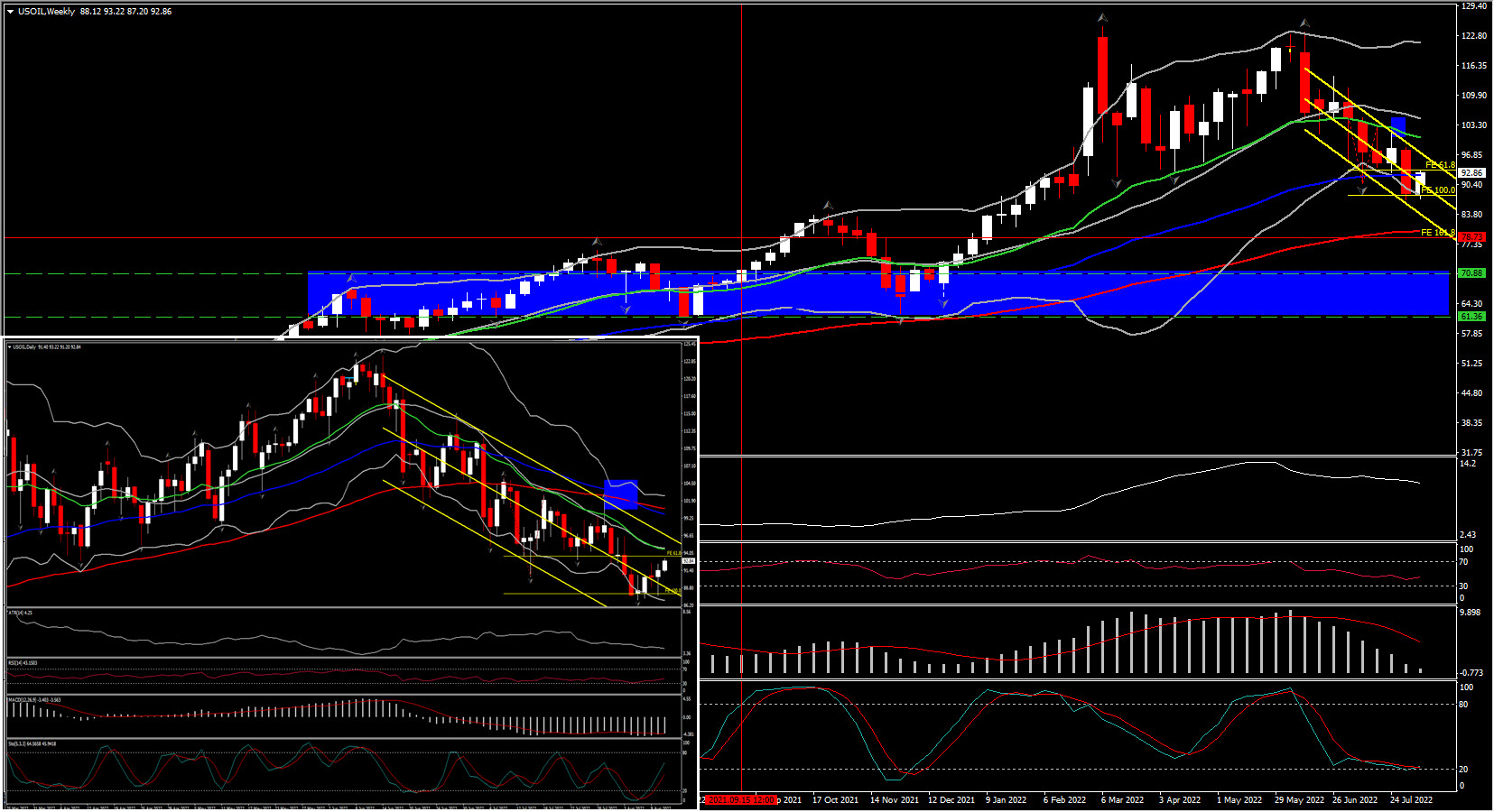

The USOIL which was below the $90 per barrel mark ahead of the US report yesterday, is now at $93 per barrel, while Brent is trading at $98.45 per barrel. The IEA highlighted that the threat of a stop in Russian gas flows has prompted a push for a shift from gas to fuel oil and that will keep demand underpinned.

From a technical perspective, the likelihood for further declines is enhanced by both the RSI and the MACD. The former has posted consecutive lower peaks however now holds at 40, while the latter remains well within its negative territory. That said, it lies above its signal line, which could imply another small bounce before an extension of the downtrend.

A return below $90 would confirm a forthcoming lower low on the daily chart, allowing the pair to flirt with its 7-month low at $86.98. In case the bears do not stop there, it will enter a drift, and the next support to consider may be the 161.8 FE at $78.70 and the 2021 triple bottom between $61.35- $70.00.

On the upside, a move confirming that the bulls have stolen all the bears’ swords – at least for a while – may see a recovery above $102.00. This could signal the rejection of the downchannel and the double top in July and may initially allow advances towards the July and June highs, at $109- $113.

Hence overall, Oil prices have remained pressured by growth concerns, which counterbalanced a disappointingly small increase in OPEC+ production targets. Reportedly, key players want to keep their reserves in case there are serious shortages over the winter, which highlights that in Europe in particular, the risk of energy rationing remains on the table. Countries are managing to fill their gas reserves, but that comes at a much higher cost.

Given that Russia is part of the wider alliance, the fact that there are preparations for a shortage indicates that key players do see the risk of severe shortages — which could signal that Russia is ready to tighten the screws on Europe even more. Indeed, Russia is already seeing strong demand from top buyers India and China, and Reuters highlighted that spot prices for Russia’s key export crude grade ESPO Blend to Asia have rebounded from all-time lows, which will limit the impact of sanctions and give Russia more options to divert supplies.

European countries meanwhile continue to struggle to top up gas storage levels, and this is coming at a cost. Reuters reported that European countries are on track to reach a gas storage filling target by the start of this winter, but also that “the cost of replenishing stocks will be over 50 billion euros ($51 billion), 10 times more than the historical average of filling up tanks for winter”. The EU is preparing for energy shortages by trying to cut back as much as possible, which means less illumination of public buildings, colder water in public swimming pools and limits for cooling down office space over the summer.

Whether that alone will be sufficient remains to be seen, and industries are also exploring gas to fuel oil switching as any rationing of gas will give private consumers and key industries a priority. TTF (EUR) and UK gas prices have dropped over the past week, but gas shortages over the winter remain a real possibility.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.