Implied Fed funds futures extended higher after the data releases that were exactly what policymakers did not want to see. The market remains priced for a 25 bp hike on March 22, with some upside risk for a 50 bp. And higher for longer remains the operative stance, with a peak of 5.5% now seen for September. At the start of February, before the hot January jobs report, the market was priced for a 4.89% peak in June.

US initial jobless claims fell -2k to 190k in the week ended February 25, again lower than expected, after dropping -3k to 192k previously. This is a seventh week under 200k, reflecting a still-tight labor market. The 4-week moving average edged up to 193k from 191.25k. Initial claims not seasonally adjusted dropped -9.3k to 201.7k after falling -14.3k to 211k (was 210.9k). Continuing claims slid -5k to 1,655k in the February 18 week after tumbling -31k to 1,660k (was 1,654k). The insured unemployment rate was steady at 1.1% for a second straight week, down from 1.2% in the prior two weeks. US Q4 nonfarm productivity growth was revised down to a 1.7% rate in the second read, a little lower than projected, from 3.0% in the Advance report. And it compares to the 1.2% (was 1.4%) Q3 rate, and the -3.8% (was -4.1%) contraction from Q2.

The slide in productivity and the jump in unit labor costs will add to worries at the FOMC that inflation will prove much more difficult to bring down (especially to 2%) and inflation expectations could be on the rise. Note that the -1.7% annual drop in productivity for 2022 is the largest decline in history (data goes back to 1947) and the first drop since 1982. Though the data have been significantly impacted by the pandemic swings, they are nevertheless bad news and reflect the massive divergence between a lean path for GDP and a robust jobs path. We still expect a 25 bp increase this month as to revert back to a more aggressive 50 bps would hurt already shaken credibility.

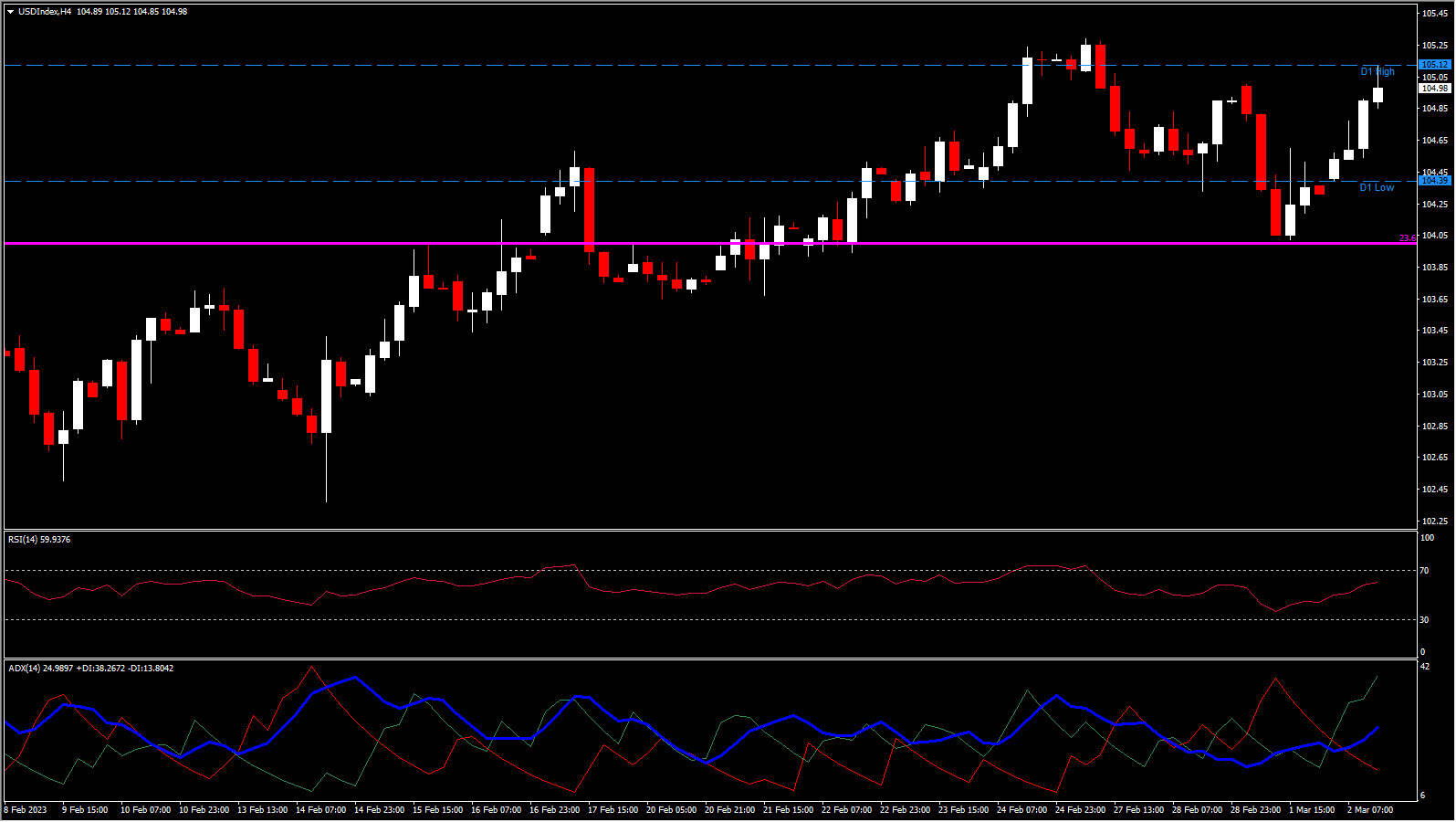

The USDindex has continued to extend higher to 105.12, after bottoming out at 104.09 yesterday. The index remains within last week’s range and while the longer term uptrend remains intact for now, the fact that the US is no longer the most hawkish of the global central banks has slowed the ascent. Eurozone core inflation data rose to a record high in the preliminary numbers for February released today, but that failed to help EURUSD, which dipped to 1.0629. Cable corrected below the 1.20 mark again, and USDJPY lifted to 136.67, which left the USDindex at 104.80.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.