GBPUSD, Daily

Markets price in 5% peak rate for the BOE. Market pricing suggests that traders expect the bank rate to reach 5% by November. This is a further shift higher following hawkish comments from MPC member Mann and hawkish comments from Powell yesterday¹. If the Fed is turning more aggressive on inflation again, it will also give European central banks cover to do more and as Mann yesterday highlighted, it could also add to pressure on Sterling, which in turn would further add to inflation risks.

The FED and Powell came out swinging, like with his Jackson Hole comments, noting that the pace of tightening may be sped up. The markets were surprised, and we saw immediate bearish reactions in bonds and stocks, with Treasury yields spiking and Wall Street slumping. The Dollar Index, on the other hand, firmed. A decision regarding an up-shift back to a half point rate hike pace on March 22 is not a done deal. Powell stressed it depends crucially on the “totality” of the upcoming data in Friday’s nonfarm payrolls, and the following CPI release on March 14.

The outlook is in line with the shift up in implied Fed funds futures. They jumped in response to Powell’s opening remarks, and now reflect about a 75% probability of a 50 basis point March increase to a 5.125% mid-rate, versus only about 25% probability before the testimony. There is approximately a 90% risk for a 5.25% to 5.5% rate in May, versus 40% previously, and a 70% risk for 5.5% to 5.75% in June, versus 30%. A terminal rate of 5.613% is seen for September, and a 5.478% rate is priced in for December.

The ECB and Lagarde have already said that another 50 bp will happen at their March meeting with consensus and a peak rate of 4.13% by October priced in. The dust should continue to settle following yesterday’s comments that indicated that the Fed could accelerate the pace of tightening moves once again. The dovish camp at the ECB may be pointing to a declining trend in headline inflation, but with global central banks fretting about the pick up in underlying inflation pressures, it will be difficult to argue for a slowdown in pace or even a pause. However, Hawks are looking at a further 50 bp in May & June and then 25 bp in July, taking the terminal rate to 4.25%.

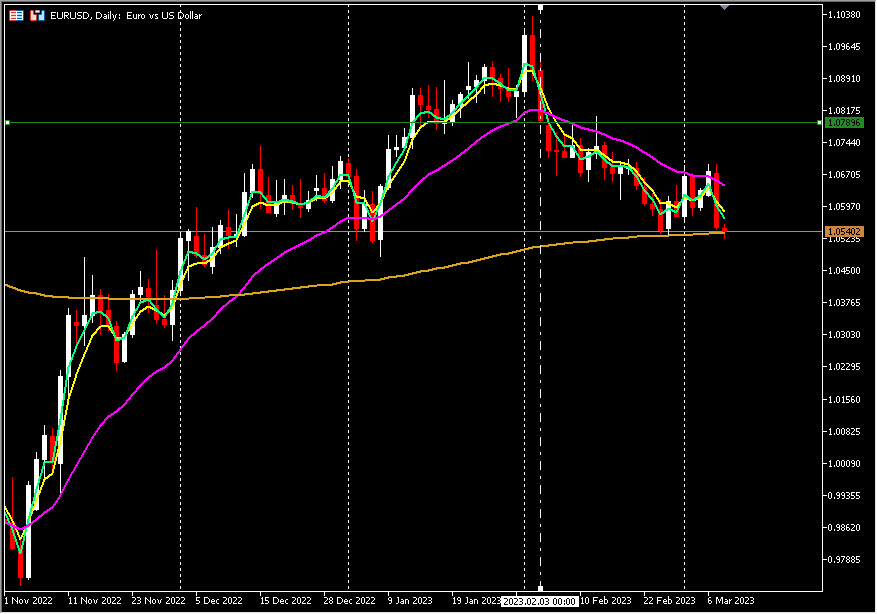

Technically, following Powell’s further Hawkish tilt yesterday, major USD crosses hit some key technical levels. USDIndex breached the 105.00 level and the daily 200-day EMA at 104.55. EURUSD descended into the 200-day EMA at 1.0530 from a test of the 1.0700 handle earlier this week. GBPUSD has been below the 200-day EMA since February 15 and breached the 200-day SMA yesterday, plotting a four month low at 1.1809 and rejection of the 1.2400 double top from mid-December and late January.

Technically, following Powell’s further Hawkish tilt yesterday, major USD crosses hit some key technical levels. USDIndex breached the 105.00 level and the daily 200-day EMA at 104.55. EURUSD descended into the 200-day EMA at 1.0530 from a test of the 1.0700 handle earlier this week. GBPUSD has been below the 200-day EMA since February 15 and breached the 200-day SMA yesterday, plotting a four month low at 1.1809 and rejection of the 1.2400 double top from mid-December and late January.

https://www.federalreserve.gov/newsevents/testimony/powell20230307a.htm¹

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.