Overnight RBA left rates unchanged at 4.1% against expectations: recent CPI and PPI data – much weaker than expected – must have weighed on the decision even if the bank stated that ”further monetary policy tightening may be required” and considers that inflation ”is to return to the target range of 2-3% by late 2025”. Keep in mind the tight local labour market. We had more bad data from China where Caixin Manufacturing shrank to contraction territory in July (49.2) and house sales figures reported the largest dip in a year. At least HSBC reported an 89% rise in pre-tax profit and is up 1.8% in HK. 10y JGB are still finding a bottom at 0.60%, Yen is tumbling and the Japanese Minister of Finance Suzuki is back to the rhetoric of ”closely monitoring the market”. US markets were up again yesterday and US500 has not had a >1% drop in 41 days now; Russell 2000 has been the monthly best performer testifying to how the rally is no longer driven only by Tech mega-caps but its breadth is broadening. This is the busiest week of the earnings season and after more than 160 companies included in the US500 have already reported, today we await Merck, Pfizer, Caterpillar, Norwegian, AMD and many more.

US500, 5 mins, Intraday Shorts covering at the close?

- FX – USDIndex is up 0.15% to 101.77, AUDUSD fell 0.74% after RBA decision (0.6668) giving up just some of yesterday’s gains, EURUSD is just shy of 1.10, Cable down 0.1% to 1.2820. USDJPY eyes 143.

- Stocks – US and EU futures are slightly red, -0.1% on average. Dax has been trading above its previous ATH seen in June for a couple of days now. Nikkei up 0.65% on weak JPY.

- Commodities – USOil extends its rally, trades at $81.52 now. Corn, Wheat fractionally up after a 5 day losing streak, Copper reacts to $400 but is surprisingly edging higher on a 2 month perspective.

- Gold – trading at $1959 this morning, XAG at $24.85.

Today: Germany, Europe unemployment, US Canada – Spain – Italy – France – Germany Manufacturing PMI, API weekly Crude Oil Stock. EARNINGS: Uber, Pfizer, Caterpillar, Norwegian BFO; AMD, Starbucks, MicroStrategy, Pinterest, ATC.

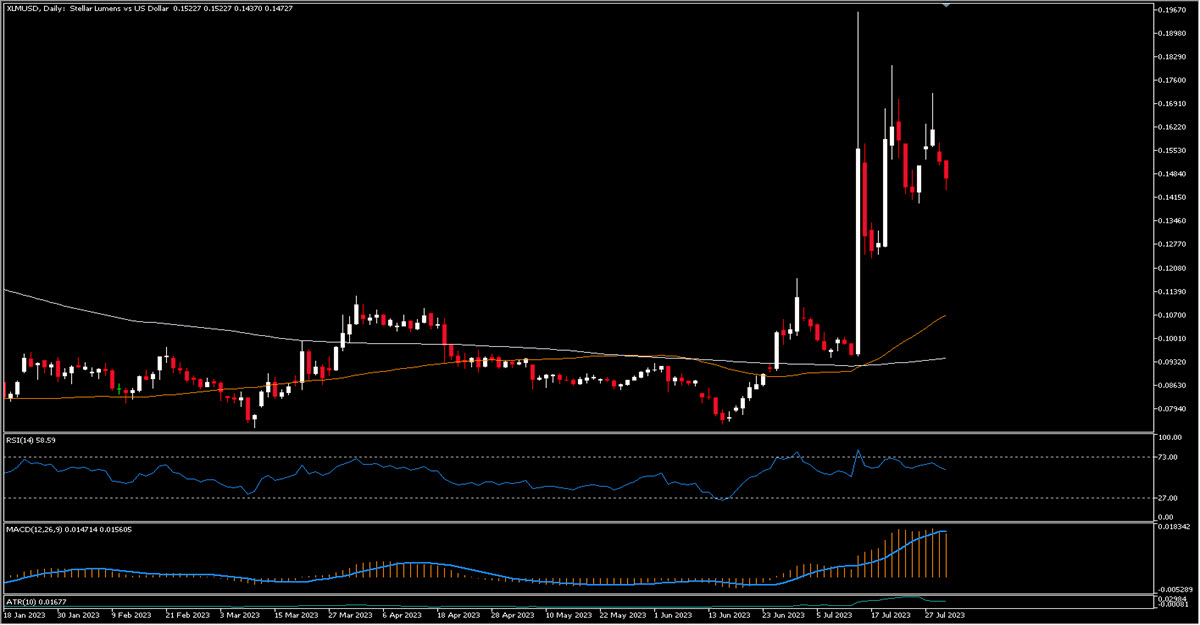

Biggest Mover: (@6:30 GMT) XLMUSD (-3.67%) trading at $0.1468 and consolidating within a triangle after the recent rally. MACD histogram just crossed to the downside, RSI negatively sloped.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.