Economic Indicators & Central Banks:

- The USDIndex tumbled to 104.12 in morning action, down from Tuesday’s 104.45, but rallied back slightly to close at 104.37.

- The Yen holds strong thanks to expectations for a BoJ rate hike next Wednesday, with USDJPY breaching 200-day EMA. The USD firmed versus CAD after the BoC’s dovish cut. The USDCAD reached April’s peak at 1.3827.

- Oil prices declined, but are once again trying to stabilize, following API data showing that US crude inventories declined by 3.9 million barrels last week. Inventories have declined for four straight weeks now. However, weak growth in top importer China and renewed optimism of a ceasefire in the Middle East have kept supply expectations underpinned. WTI is currently trading at USD 77.38 per barrel, Brent at USD 81.49 as markets wait for the official U.S. inventory report.

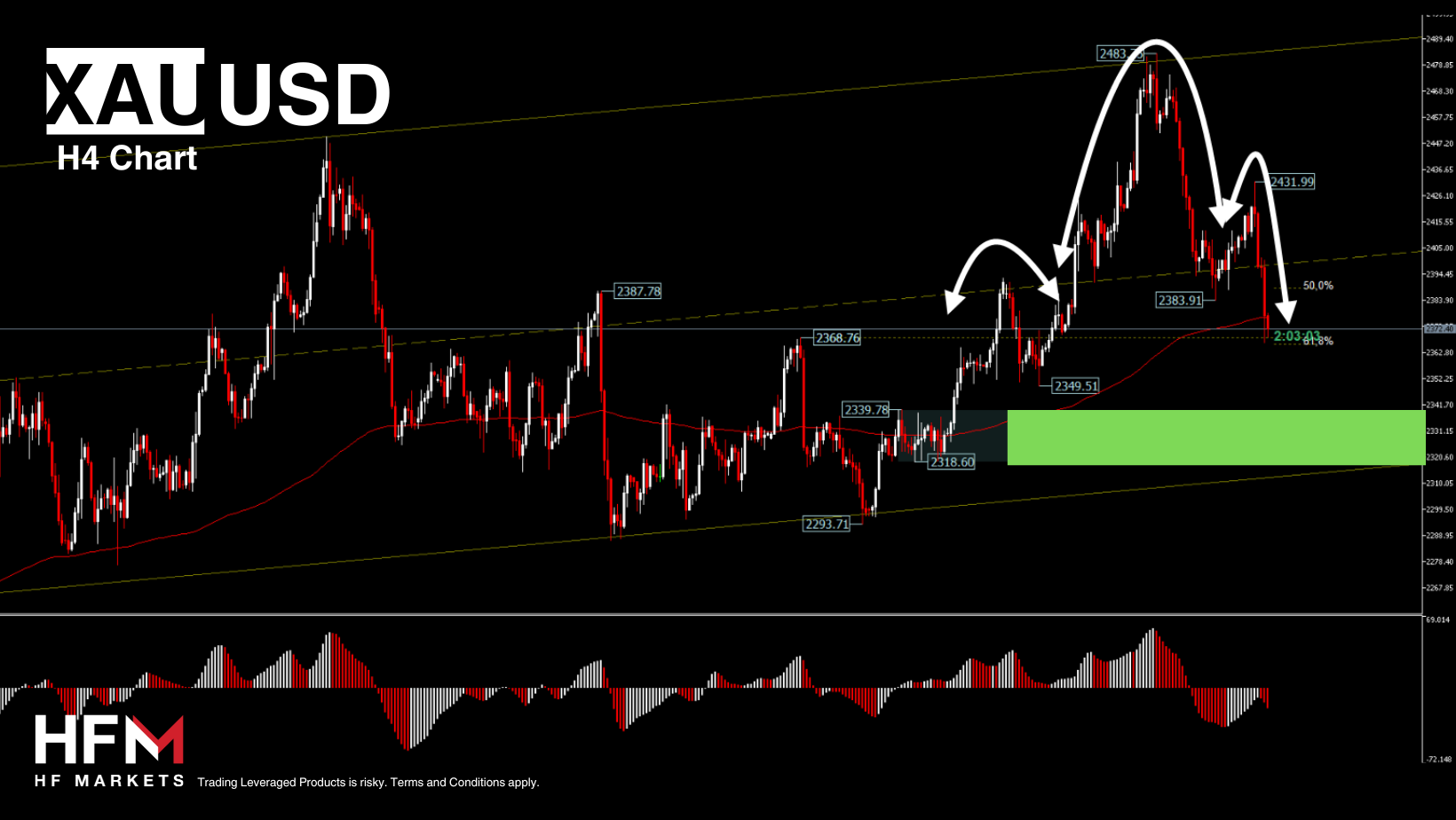

- Gold is down to $2370 a two-week low. The downfall could be attributed to some technical selling, though it is expected to be limited, considering the fundamentals, such as Fed’s cut and the risk-off mood which could support Gold ahead of the US data.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.