EURUSD, H1

US headline CPI increased 0.4% in February and the core rose 0.5%. The data are close to expectations though the latter is a little hotter than expected. These follow respective gains of 0.5% and 0.4%, in January and 0.1% and 0.4% in December. The 12-month headline pace slid to 6.0% y/y from 6.4% y/y, while the core rate was 5.5% y/y from 5.6% y/y. The deceleration in both is good news for the FOMC.

Meanwhile, Bloomberg reported Powell’s “super core” rose 0.5% versus 0.36% previously. For the guts of the report:-

- Energy prices dipped -0.6% after bouncing 2.0% previously. However, gas prices rose 1.0% after January’s 2.4% rebound.

- Services prices were up 0.5% versus the 0.6% gain and are at a 7.6% y/y pace.

- Housing rose 0.5% after the prior 0.8% gain, but owners’ equivalent rent, now one of the focal points for the Fed, increased another 0.7%, the same as in January.

- Transportation costs edged up 0.2% from 0.4%. New vehicle prices were up 0.2%, versus 0.2% previously. Used car prices dropped -2.8% from -1.9%. Airline fares surged 6.4% from -2.1%.

- Food/beverage prices rose 0.3% from 0.5%.

- Apparel prices increased 0.8% from 0.8% previously. Recreation climbed 0.9% from 0.5%.

- Education inched up 0.1% from 0.4%. And commodity prices were up 0.2% from 0.4%.

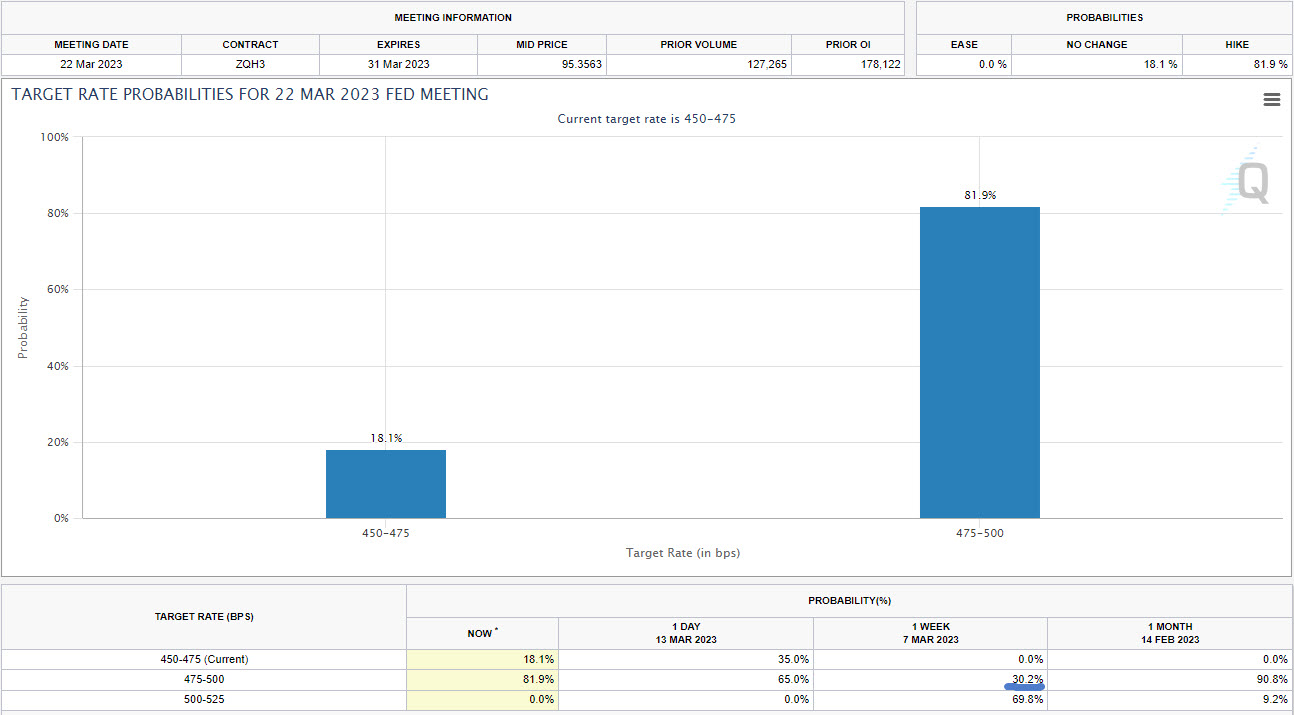

The Fed Funds Futures from the CME is now pricing in a 81.95% chance of a 25 bp interest rate hike next week from the FOMC, up from 75% before the CPI data, and only 30.2% a week ago, ahead of NFP and the SVB and Signature Bank debacle.

Treasury yields are mixed but shorter rates are on the rise, giving back some of the massive flight to safety demand. Rates inched up on the CPI release but only briefly. Most of the inflation numbers decelerated to give the FOMC some wiggle room. It looks like a hike is still on the agenda, assuming stable financial conditions next week. But today’s numbers avoid the potential 50 bp boost Chair Powell put on the table in last Tuesday’s testimony. It does look like the FOMC can stay the course with a 25 bp hike. The 2-year yield is up 24.5 bps at 4.223% after having traded just below 4% overnight. The 10- and 30-year yields are about 1.7 bps lower at 3.556% and 3.707%, respectively. The curve is at -66 bp. Wall Street is rallying with the futures firmly in the green. The US500 is up 1.27%, while the US100 is 1.22% higher, and the US30 rising 1.05%. The USDIndex has fallen to 103.500 from an high of 104.049 and EURUSD holds over 1.0700 but below yesterday’s high of 1.0748 and trades at 1.0730.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.