I know I’ve talked a lot about Australia (notably here and here), so I had decided I would stop for a while. Nevertheless, it is time to resume as recent data releases point to what these previous posts were suggesting: construction and banking are not performing well in the country.

The first is easy to see: the AiG Performance of Construction Index has been registering numbers below 50 since October, moving lower every month, reaching 44.5 in December. Naturally, this is not the first time real estate in the country has underperformed, as it registered similarly low numbers in 2011-2013, without any significant effects on the economy. However, construction work completed is also facing problems, with negative growth rates recorded as of late 2015.

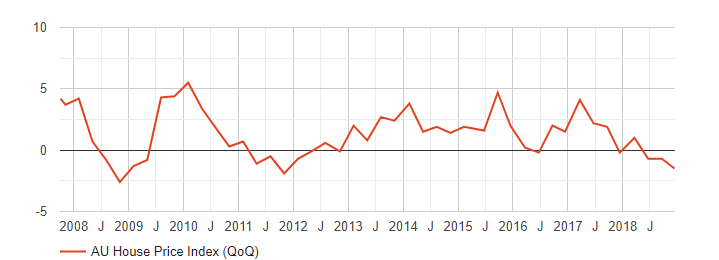

House Prices are also going down, also registering three consecutive quarters of negative (increasing) growth rates. Was this also a feature of the past, especially of the 2011-2013 period when construction underperformed? Yes, three quarters of negative growth were also observed, however, with the movement being much less persistent. Still, one could buy the argument that this has happened before and there is no need to worry.

Then what about home loans? In 2018, 8 out of 11 available months registered negative growth rates, compared to 6 last year, which more or less meant that the amount of lending remained relatively stable. The major difference between those previous times is that the reduction appears to be more persistent, while large one-off changes in the stock of loans (perhaps related to early repayments) were the drivers in the past. A similar case can also be made for Investment Lending for Homes in the country.

Australia has an additional issue related to lending, and this is called negative gearing. In simple words, negative gearing suggests that someone could buy a house, rent it for less than the interest payments and offset the negative difference by deducting it from their tax statement. This policy is usually used by middle-income and lower-income people, however, the issue is that one needs to be able to cover a substantial percentage of their mortgage payments with the rental income, otherwise there would be no incentive to pursue such a strategy. As interest rates are rising, rents will have to increase in order to cover for these changes, hence bringing people to the point of wondering whether it would be easier to rent smaller properties. This would affect prices, especially for owners of large properties.

Ironically, the Deputy Governor of RBA has actually acknowledged the fact that housing conditions are deteriorating. In his own words, Guy Debelle suggested that “While not directly related to the housing measures, there has been some tightening in credit for developers of residential property. (…) That is, banks are less willing to lend given the fall in prices. (…) Housing prices have fallen by almost 5 percent from their late 2017 peak while the pace of housing credit growth has slowed over the past couple of years.” In essence, Debelle has been suggesting that lower lending is causing lower house prices, forming a self-fuelled cycle. As part of the global fixation on inflation “having” to be close to 2%, RBA currently faces a situation where a recession may occur with the policy rate standing at 1.5%, leaving it with very little room to manoeuvre, using traditional policy instruments.

Nonetheless, as suggested in the earlier posts, more time is required to see when a recession will hit the country, with this analyst’s forecast being that mid-2019 will be the time to really tell what will go on.

Click here to access the HotForex Economic Calendar

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.