USDIndex gained +0.27% and posted a 1-month high. Higher T-note yields on Wednesday supported modest gains in the Dollar. In addition, the S&P 500’s decline to a 5-week low and the Yuan’s weakening to a 9-month low amid concerns about China’s economy fuelled liquidity for the Dollar. Dollar gains accelerated when the minutes of the July FOMC meeting stated that inflation risks allow for more rate hikes.

Wednesday’s US economic news was mixed for the Dollar. On the bullish side, July new housing starts rose +3.9% m/m to 1.452 million, stronger than expectations of 1.450 million. July manufacturing production unexpectedly rose +0.5% m/m, stronger than expectations of no change. In contrast, July building permits, a proxy for future construction, rose +0.1% m/m to 1.442 million, weaker than expectations of 1.463 million.

The yield on the US 10-year Treasury rose past the 4.25% mark, the highest since November 2007 as markets are still concerned about prolonged tight monetary policy. Minutes from the latest FOMC meeting showed broad consensus over a 25bps rate hike. Yields also remained higher on concerns of higher bond supply, after the government increased the amount of bonds auctioned earlier in the month.

The impact of the rising Dollar and global bond yields pressured commodity prices. Gold closed down -0.35%, Silver closed down -0.53%. Precious metals prices on Tuesday gave up early gains and moved lower, with Gold falling to a 7-week low. Silver prices also fell, after JPMorgan Chase and Barclays cut China’s 2023 GDP estimates, a bearish sign for industrial metal demand. Copper fell -0.30%, Palladium fell -2.2% and Platinum -0.49%.

Precious metals initially moved higher, as the deepening liquidity crisis in China fuelled safe-haven demand for precious metals after Zhongrong International Trust missed payments on dozens of its investment products. Silver prices found early support on signs of strengthening industrial metals demand after Wednesday’s news showed June eurozone industrial production and July US manufacturing output rose more than expected.

Technical Review

What happens in China continues to correlate strongly with copper prices. In fact, there were significant rallies after the Chinese government announced additional policy support, however unfavourable economic data ultimately dominated and led to a significant sell-off. The PBoC finally decided to cut interest rates yesterday, but Copper prices fell further. The rate cut was followed by a series of very poor data, so the market may have wanted more.

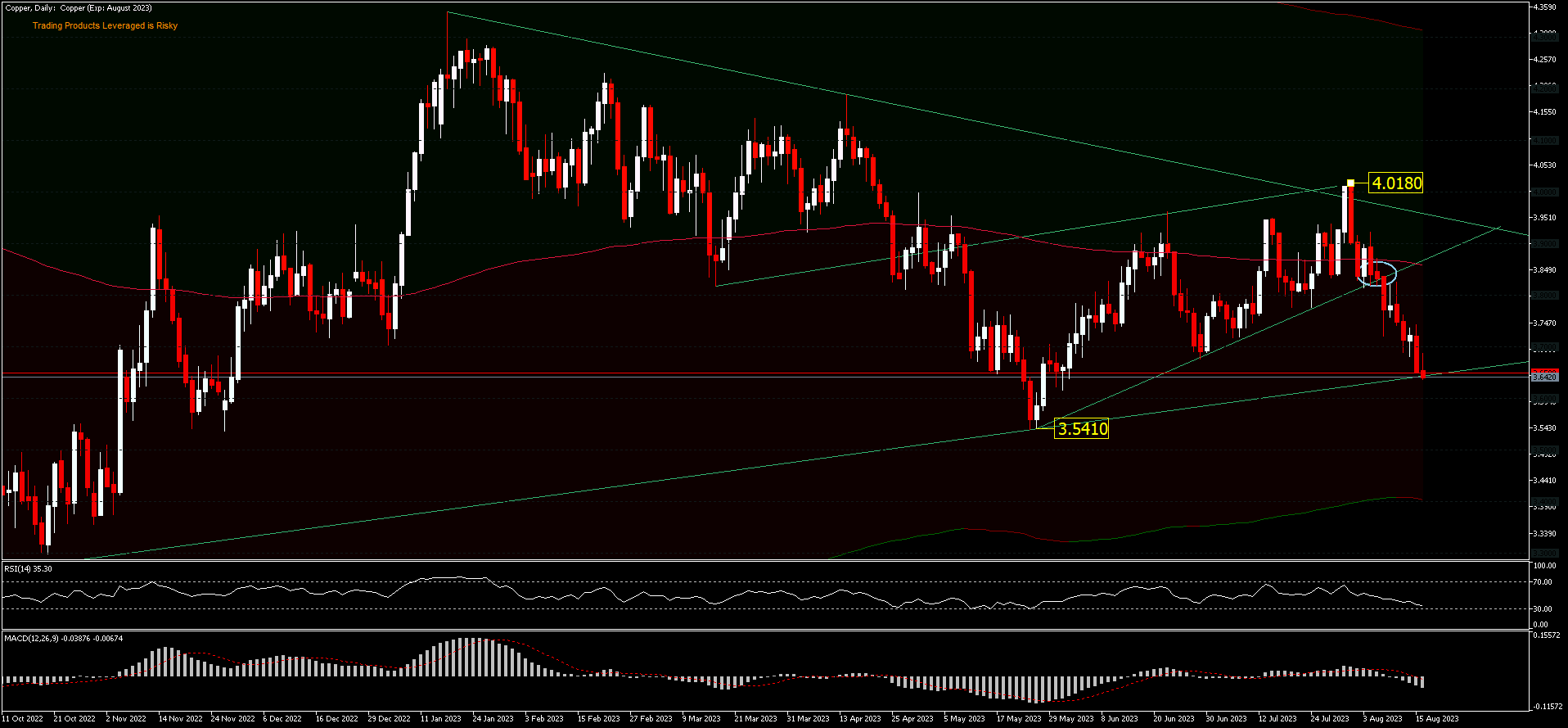

Copper, D1 – is seen resuming the decline of 4.018 and is now sitting on a major trendline which acted as support earlier, and a break below it will open the door for a drop to 3.5410/FE61.8% (3.5175) level. A move below this level could send Copper to lower levels with projections for FE100% at 3.2081 (from 4.3490-3.5410 and 4.0180 pullback). The current price position is below the 200-day EMA, and Copper continues to fall with very shallow pullbacks along the way. RSI looks close to oversold levels, but MACD still continues to be in the selling zone.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.